Publicado

Employment and taxes in Latin America: An empirical study of the effects of payroll, corporate income and value-added taxes on labor outcomes

Empleo e impuestos en América Latina: un estudio empírico de los efectos de los impuestos a la nómina, la renta de los negocios y al valor agregado en el mercado de trabajo

Emprego e impostos na América Latina: Um estudo empírico dos efeitos dos impostos sobre a folha de pagamento, a renda dos negócios e sobre o valor agregado no mercado de trabalho

DOI:

https://doi.org/10.15446/cuad.econ.v35n67.52580Palabras clave:

VAT, payroll tax, corporate income tax, employment, informality, wages, Latin America (en)impuesto al valor agregado, impuesto a la nómina, impuesto a la renta de los negocios, empleo, informalidad, salarios, América Latina (es)

Imposto sobre o valor agregado, imposto sobre a folha de pagamento, imposto sobre a renda dos negócios, emprego, informalidade, salários, América Latina (pt)

Este artículo explora de manera empírica los efectos de los impuestos a la nómina, al valor agregado y a la renta de los negocios en una serie de variables del mercado de trabajo tales como participación laboral, empleo, informalidad y salarios. Los resultados, con datos para 15 países de América Latina, sugieren que los efectos de cada impuesto son marcadamente diferentes y dependen de diversos aspectos de las instituciones laborales y tributarias. Los impuestos a la nómina reducen el empleo e incrementan los costos laborales cuando sus beneficios no son valorados por los trabajadores; pero cuando son valoradas pueden elevar la participación laboral sin incrementar los cotos laborales. Los impuestos al valor agregado aumentan la informalidad y reducen la demanda de fuerza de trabajo calificada. En contraste, los impuestos a la renta de las empresas pueden ayudar a reducir la informalidad, especialmente entre trabajadores con bajo nivel educativo; sin embargo, cuando las capacidades de administración tributaria son fuertes estos impuestos pueden reducir la participación laboral y el empleo de trabajadores de nivel educativo medio y avanzado.

https://doi.org/10.15446/cuad.econ.v35n67.52580

Employment and taxes in Latin America: An empirical study of the effects of payroll, corporate income and value-added taxes on labor outcomes

Empleo e impuestos en América Latina: un estudio empírico de los efectos de los impuestos a la nómina, la renta de los negocios y al valor agregado en el mercado de trabajo

Emploi et impôts en Amérique latine : une étude empirique des effets des impôts sur la masse salariale, le revenu des affaires et la valeur ajoutée sur le marché du travail

Emprego e impostos na América Latina: Um estudo empírico dos efeitos dos impostos sobre a folha de pagamento, a renda dos negócios e sobre o valor agregado no mercado de trabalho

Eduardo Loraa

Johanna Fajardo-Gonzálezb

a Center for International Development, Harvard University. Massachusetts, United States. E-mail: eduardo_lora@hks.harvard.edu

b Department of Applied Economics, University of Minnesota. Minnesota, United States. E-mail: fajar016@umn.edu

Sugerencia de citación: Lora, E., & Fajardo-González, J. (2016). Employment and taxes in Latin America: An empirical study of the effects of payroll, corporate income and value-added taxes on labor outcomes. Cuadernos de Economía, 35(67), 75-117. doi: 10.15446/cuad.econ.v35n67.52580.

The authors acknowledge valuable support and advice from Carmen Pagés. Useful comments were received from Ana Corbacho, Santiago Levy, ángel Melguizo, José Antonio Ocampo, Teresa Ter-Minassian, participants of internal workshops at the Inter-American Development Bank, and two anonymous referees.

Abstract

This paper empirically explores the effects of payroll taxes, value-added taxes and corporate income taxes on a variety of labor market outcomes such as participation, employment, informality, and wages. The results are based on nationallevel data of labor variables for 15 Latin American countries, and indicate that the effects of each tax are markedly different and may depend on several aspects of labor and tax institutions. Payroll taxes reduce employment and increase labor costs when their benefits are not valued by workers, but otherwise may increase labor participation and not raise labor costs. Value-added taxes increase informality and reduce skilled labor demand. In contrast, corporate income taxes may help reduce informality, especially among low education workers, but when tax enforcement capabilities are strong they may reduce labor participation and employment of medium- and high-education workers.

Keywords: VAT, payroll tax, corporate income tax, employment, informality, wages, Latin America.

JEL: J21, J30, J32, H24, H25.

Resumen

Este artículo explora de manera empírica los efectos de los impuestos a la nómina, al valor agregado y a la renta de los negocios en una serie de variables del mercado de trabajo tales como participación laboral, empleo, informalidad y salarios. Los resultados, con datos para 15 países de América Latina, sugieren que los efectos de cada impuesto son marcadamente diferentes y dependen de diversos aspectos de las instituciones laborales y tributarias. Los impuestos a la nómina reducen el empleo e incrementan los costos laborales cuando sus beneficios no son valorados por los trabajadores; pero cuando son valoradas pueden elevar la participación laboral sin incrementar los cotos laborales. Los impuestos al valor agregado aumentan la informalidad y reducen la demanda de fuerza de trabajo calificada. En contraste, los impuestos a la renta de las empresas pueden ayudar a reducir la informalidad, especialmente entre trabajadores con bajo nivel educativo; sin embargo, cuando las capacidades de administración tributaria son fuertes estos impuestos pueden reducir la participación laboral y el empleo de trabajadores de nivel educativo medio y avanzado.

Palabras clave: impuesto al valor agregado, impuesto a la nómina, impuesto a la renta de los negocios, empleo, informalidad, salarios, América Latina.

JEL: J21, J30, J32, H24, H25.

Résumé

Cet article explore de manière empirique les effets des impôts sur la masse salariale, la valeur ajoutée et le revenu sur les affaires dans une série de variables du marché du travail comme la participation de la main-d'œuvre, l'emploi, l'informalité et les salaires. Les résultats, selon des données pour 15 pays d'Amérique latine, indiquent que les effets de chaque impôt sont notablement différents et dépendent de divers aspects des institutions professionnelles et fiscales. Les impôts sur les salaires réduisent l'emploi et augmentent les coûts du travail quand leurs avantages ne sont pas valorisés par les travailleurs mais quand ils le sont, ils peuvent élever la participation professionnelle sans en augmenter les coûts. Les impôts à la valeur ajoutée augmentent l'informalité et réduisent la demande de force de travail qualifié. Par contre, les impôts sur le revenu des entreprises peuvent aider à réduire l'informalité, en particulier chez les travailleurs d'un faible niveau d'instruction ; cependant, quand les capacités de l'administration fiscale sont fortes, ces impôts peuvent réduire la participation de la main-d'œuvre et l'emploi de travailleurs d'un niveau d'éducation moyen ou élevé.

Mots-clés : impôt sur la valeur ajoutée, impôt sur la masse salariale, impôt sur le revenu des affaires, emploi, informalité, salaires, Amérique latine.

JEL: J21, J30, J32, H24, H25.

Resumo

Este artigo explora, de maneira empírica, os efeitos dos impostos sobre a folha de pagamento, sobre o valor agregado e sobre a renda dos negócios em uma série de variáveis do mercado de trabalho tais como participação trabalhista, emprego, informalidade e salários. Os resultados, com dados para 15 países da América Latina, sugerem que os efeitos de cada imposto são notadamente diferentes e dependem de diferentes aspectos das instituições trabalhistas e tributárias. Os impostos sobre a folha de pagamento reduzem o emprego e aumentam os custos trabalhistas quando os seus benefícios não são valorizados pelos trabalhadores; mas, quando são, podem elevar a participação trabalhista sem aumentar os custos. Os impostos sobre o valor agregado aumentam a informalidade e reduzem a demanda de força de trabalho qualificada. Em compensação, os impostos sobre a receita das empresas podem ajudar a reduzir a informalidade, especialmente entre trabalhadores com baixo nível acadêmico; no entanto, quando as capacidades de administração tributária são fortes, estes impostos podem reduzir a participação trabalhista e o emprego de trabalhadores de nível acadêmico médio e avançado.

Palavras-chave: Imposto sobre o valor agregado, imposto sobre a folha de pagamento, imposto sobre a renda dos negócios, emprego, informalidade, salários, América Latina.

JEL: J21, J30, J32, H24, H25.

Este artículo fue recibido el 18 de noviembre de 2014, ajustado el 2 de marzo de 2015 y su publicación aprobada el 3 de marzo de 2015.

INTRODUCTION

Over the past 20 years, Latin American tax systems have undergone substantial transformations. The process began with trade liberalization, which saw import tariffs slashed and prompted governments to strengthen alternative revenue sources, particularly value-added taxes (VAT). VAT has become common in Latin America, as in most of the developing world, and now raises about a third of fiscal revenues. General VAT tax rates have increased from an average of 12.1% in 1985 (in the 13 countries with VAT systems) to 14.8% in 2009 (in 18 countries)1.

In parallel with this process, there have been important changes in social security and social protection systems, due to the maturation of traditional pay-as-you-go pension programs and their total or partial replacement by fully funded defined contribution systems in several countries, the extension of health insurance programs, and the creation of a diversity of social protection programs. A significant proportion of the additional revenues required by these systems are currently levied by a variety of payroll taxes and contributions, which either did not exist 20 years ago or were substantially lower (taxes and contributions on the payroll increased from an average of 21% in 1985 to 24.3% in 2009).

In contrast to these changes, income taxes have remained relatively constant since the mid-1980s, at least in terms of the revenues generated (around 4% of GDP). Nonetheless, the maximum rates of corporate income tax have fallen from 44% in 1985 to about 30% since the mid-1990s and that of individual income tax from 50% in 1985 to around 30% since the mid-1990s. Furthermore, the bases, exemptions and other features of the taxes have been the subject of continuous adjustments in most countries (Lora, 2012).

The effects of all these changes on employment and wages are still poorly understood. While an extensive theoretical and empirical literature has studied the labor effects of trade taxes, and to some extent payroll taxes, a comparable effort is still wanting with respect to VAT and corporate income taxes.

This paper reviews the theoretical and empirical literature on the labor effects of taxes and empirically explores the effects of payroll taxes, VAT and corporate income taxes. It uses national-level data of labor variables for 15 Latin American countries processed in a homogeneous way from household surveys, avoiding the methodological limitations and discontinuities of other sources.

With respect to payroll taxes, this paper confirms some of the findings of previous literature, such as their deleterious effects on employment, and expands on an important aspect of those taxes that has been recognized by the theoretical literature but has been largely neglected by empirical works: the different effects of payroll taxes that give the taxed workers access to benefits compared with those that are pure taxes.

Value-added taxes are often considered less distortive than other taxes because they affect all sectors and factors in a more homogeneous way. However, our results suggest that the effects of VAT on labor outcomes differ strongly according to the skill level of the workers, a result that seems to be the consequence of the presence of large informal segments and the different degrees to which unskilled and skilled labor can be substituted by capital.

Our findings on corporate income tax reaffirm the conclusion that unskilled and skilled workers may be affected differently by taxes and that the effects are mediated by institutional factors such as tax collection capabilities, minimum wages, and the degree of labor flexibility allowed by the labor code.

The rest of this paper is organized as follows. The next section is devoted to a review of the theoretical and empirical literature on the labor effects of payroll, VAT and corporate income taxes. This is followed by the analytical framework that will be used to interpret the empirical results. The data sources are then described in detail, as is the econometric approach. The subsequent sections discuss the empirical results, before offering conclusions and suggestions for further research.

LITERATURE REVIEW

The Labor Effects of Payroll Taxes2

In theory, the effects of payroll taxes on employment, unemployment and wages are ambiguous (Gruber, 1997, and Kugler & Kugler, 2009, provide theoretical models). Unlike other taxes, most payroll taxes entitle workers to a set of benefits. Changes in payroll taxes can be fully shifted from firms to employees in the form of lower wages with no loss on employment when workers value the benefits as much as the cost of the contributions for themselves and their employers. On the other hand, if payroll taxes finance benefits not completely accrued by employees, there will be only partial shifting and employment is likely to be affected. The extent of shifting also depends on the elasticities of labor demand and supply. Higher labor demand elasticity increases the pass-through and reduces the impact on employment, but higher labor supply elasticity has the effect of reducing the extent of pass-through and increasing the impact on employment. In addition, the ability to pass on payroll taxes as lower wages will depend on the extent to which there are downward wage rigidities (for example, due to minimum wages or union-bargained wages).

In general, the theoretical models predict that the magnitude of the impact of payroll taxes on employment depends on how much workers value the benefits received from those taxes, and on the degree of wage rigidity. If workers do not fully value benefits and there is some degree of wage rigidity, higher payroll taxes will probably decrease employment and increase unemployment. In the presence of informality, formal sector employment is likely to fall.

These theoretical predictions have been assessed both with aggregate data and with micro-level data. Most of the studies that use aggregate data refer to developed countries, and have confirmed the theoretical predictions3. The only study that has included country-level data from Latin American countries, Heckman & Pagés (2004), lends strong support to the theoretical prediction that, with partial shifting of social security contributions to wages, employment falls. They found that the pass-through of higher social security contributions on wages in Latin America was 36% and that a 10% increase in contributions reduced employment by 4.5%.

The findings of a growing number of empirical studies for developed countries that rely on micro-data are also mostly consistent with the theoretical predictions. These studies do not suffer from the two main potential weaknesses of those based on aggregate data, namely reverse causality, as labor outcomes may influence tax rates, and omitted variable bias, as payroll tax rates across countries may be correlated to other institutional factors that also relate to labor outcomes. The studies, surveyed by Melguizo (2009), consistently indicate that payroll taxes are partially shifted to workers in the form of lower salaries, and that the effect is stronger in the longer run and depends on the institutional features of labor markets and the type of taxes.

Evidence for Latin America is still limited, but growing. Gruber (1997) assessed the effects of some payroll tax changes in Chile that were not applied uniformly across different types of firms. He found no effect at all on employment, consistent with the fact that the additional labor costs were fully shifted to workers, given the strong connection between contributions and benefits. In a similar way, Cox Edwards (2002), differentiating between workers that contributed to the new Chilean pension system and those who did not, found full shifting for women and partial shifting for men. Cruces, Galiani and Kidyba (2010) examined the changes in payroll taxes in Argentina across regions in the 1990s. They found no effect on employment, and that 55% of the payroll tax was shifted to workers. Kugler & Kugler (2009) examined the effects of changes in payroll taxes in Colombia and found that a 10% increase in payroll taxes lowered formal employment in the manufacturing sector by between 4% and 5%, and reduced wages by between 1.4% and 2.3%. The low shifting in Colombia is likely to be the result of weak linkages between benefits and taxes and the presence of downward wage rigidities induced by a binding minimum wage.

The theoretical prediction that payroll taxes encourage informality has found support in a few studies for Latin American and other developing countries. A study for Colombia showed that a 10% increase in non-wage labor costs increased informality by 8%.

Labor Effects of VAT

A flat tax levied on the value added in each of the production and distribution stages of all consumption goods is considered less distortive than other taxes that are levied on only some stages, some goods or some types of income because it does not affect production or investment decisions by firms.

The distinctive feature of VAT is that is paid by firms on the value added at each production stage, based on the difference between total sales and total input costs. The main difference between a VAT and a retail sales tax lies in the way it is collected and in who remits the tax to the government, a difference thought to create significant incentives to reduce tax evasion (Slemrod, 2008). Firms have an incentive to ask their suppliers for accurate receipts because they can deduct input taxes from their own VAT bill. In developing countries, where informality is pervasive, the self-enforcing nature of VAT is appealing to governments and tax administration offices, and no doubt this has contributed to its adoption throughout the world (Keen & Lockwood, 2010), from 47 countries in 1990 to over 140 today (Bird & Gendron, 2007).

However, the VAT may induce further informality because its self-enforcing nature applies only to firms operating in the formal sector. For those firms that escape the tax radar, the VAT may be an additional reason to stay informal4. The implications for informality of the credit method of collection of VAT have been modeled and empirically tested by De Paula and Scheinkman (2010). Their model exploits the idea that collecting value-added taxes according to a credit scheme sets in motion a mechanism for the transmission of informality. Since purchases from informal suppliers do not generate tax credits and informal buyers cannot use tax payments from formal suppliers, there is an incentive for informal firms to deal with other informal firms. Firms that evade taxes have to pay fines, and the probability of this occurring increases with firm size. Therefore, firms trade off the cost of paying taxes versus the scale limitations of becoming informal5. De Paula and Scheinkman's empirical analysis used data for around 48,000 small firms in Brazil and showed that, in fact, various measures of supplier and purchaser formality are correlated with the formality of a firm6.

Apart from the work by De Paula and Scheinkman (2010), there is a dearth of empirical studies on the effects of VAT on informality and other labor outcomes.

While some previous works have uncovered evidence that higher tax rates induce informality (Friedman et al., 2000; Johnson, Kaufmann & Shleifer, 1997), none has focused on VAT.

Labor Effects of Corporate Income Taxes

Research on the labor market implications of corporate taxation is scant, both in the developed and the developing world. Yet, through their indirect effect on labor demand, corporate taxes may affect employment and wages and may contribute to informality and involuntary unemployment. Any increase in the cost of capital, including taxes, can affect the labor market by reducing output, by inducing factor substitution, and by reducing labor productivity. The higher cost of capital due to a corporate tax will increase production costs and lead to a fall in output, thereby decreasing the demand for both capital and labor. However, the increase in the relative price of capital with respect to labor will favor the relative demand for labor, partly offsetting the former effect. Finally, lower levels of capital will reduce the productivity of workers, leading to a fall in the wage rate. Corporate income tax may also result in some production moving from the formal to the informal sector, increasing demand for labor in the latter, and at least partially countering the negative effect on employment in the formal sector. The overall effect on employment in the economy will depend on the relative labor intensities between the two sectors and the substitutability of labor and capital (see OECD, 2011, for further elaboration and references).

Empirical research on these theoretical predictions is still very limited, both in developed and developing countries7. Chile has been the subject of some of the few studies. Martínez, Morales, and Valdés (2001) assessed the employment effect of corporate taxes through potential complementarities. They concluded that the labor to cost of capital elasticity is near 0.2, implying that, by increasing the cost of capital, a higher corporate tax rate should depress labor demand. Cerda and Larraín (2010), using firm level data from Chile for 1981-96 (a period of high volatility in corporate income tax rates), found that corporate income taxes reduced the demand for labor due to its complementarity with capital. A 1% increase in corporate income tax revenue reduced labor demand by 0.2%. Of special interest is the asymmetric effect of taxation according to company size. The impact on labor demand was significantly higher in large corporations than in small enterprises, while the demand for capital was more responsive to corporate tax changes in small firms (being less credit constrained, larger firms are more easily able to cover the high costs of firing workers). It should be noted that the dataset used in this study included only registered firms with more than 10 employees, and therefore its findings did not address the impact of corporate income taxes on microsize firms and independent workers (which are identified with informality in our empirical work below). Presumably, by shifting labor from larger to smaller firms, corporate income tax may have deleterious effects on the formal/informal composition of employment, a topic that has been studied empirically by Loayza (1996). Using data from Latin American countries in the early 1990s, Loayza found that the size of the informal sector depends positively on the maximum corporate income tax rate. His results also confirmed the importance of the quality of government institutions for discouraging informality. Vuletin (2008) built on Loayza's work, including corporate income taxes as part of a tax burden variable which was found to be causally related to informality.

RESEARCH OBJECTIVE AND ANALYTICAL FRAMEWORK

As the previous section makes clear, the effects of taxation on labor outcomes are still poorly understood. Even in the case of payroll taxes—which have been the focus of a large body of literature—only a few Latin American countries have been studied. The effects of valued-added and corporate income taxes on employment, informality and wages in Latin America are largely unknown. The objective of this paper is to provide a broad empirical assessment of the effects on labor outcomes of payroll, value-added and corporate income taxes in Latin American economies. More specifically, we are interested in assessing how taxes affect labor participation, occupation, informality and wages. For this purpose we make use of a unique database that covers 15 Latin American countries in a consistent way since the early 1990s, described below. Needless to say, ours is an ambitious objective, which will provide only incomplete responses and will leave many questions unanswered. However, it will hopefully offer a general indication of the labor effects that different taxes have, depending on the type of workers (skilled versus unskilled, formal versus informal) and several features of the economy (such as the ability of the government to enforce the tax code and the minimum wage level, among many other things). Taxes and informality are closely related phenomena because the possibility of not paying taxes is an important motivation for individuals or businesses to operate in the informal sector. Although payroll taxes are often assumed to be one of the main culprits behind labor informality, there is no conclusive evidence that supports this, since the labor effects of valued-added and corporate income taxes are very poorly understood. Informal workers will be defined here as those who either work in a small firm, or are self-employed or unpaid workers.

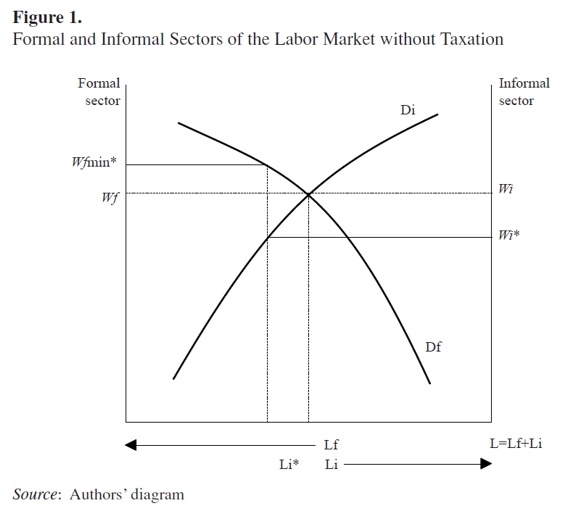

Since our empirical effort will try to deal with the effects of taxes on several labor outcomes, it is important to first provide a simple analytical framework that describes the relationships between the labor variables under consideration (taken from Levy, 2008, pp. 142-155). The basic framework will be presented here, while its application to each tax under consideration will be shown in parallel with the discussion of the econometric results below. Figure 1 represents the labor market of a developing economy, assuming that the labor supply, which is fixed at L, is Employment and taxes in Latin America Eduardo Lora y Johanna Fajardo 47 fully occupied in the formal and informal segments of the labor market (initially, L = Lf + Li). Each segment has its own labor demand, which depends on the capital stocks and the technologies used in each sector, and which is assumed to be consistent with profit maximization. Labor demand in the informal segment (Di) is drawn from right to left. At equilibrium, if there are no wage rigidities, wages in both segments are the same (wf = wi), since workers are assumed to move freely between them. If a binding minimum wage (wfmin*) is introduced in the formal segment, informality will increase to Li*, and informal wages will fall to wi*. In this simplified model, there will be no involuntary unemployment. Like a minimum wage, any of the three taxes considered will affect the demand for formal labor because firms are responsible for their payment and taxes affect their profit maximizing position. Any change in the demand for formal employment will have repercussions on formal wages and on the allocation of the labor force between formal and informal activities. In addition, however, some taxes may affect the total supply of labor. For instance, a payroll tax that generates important benefits to some workers may encourage labor participation.

DATA SOURCES

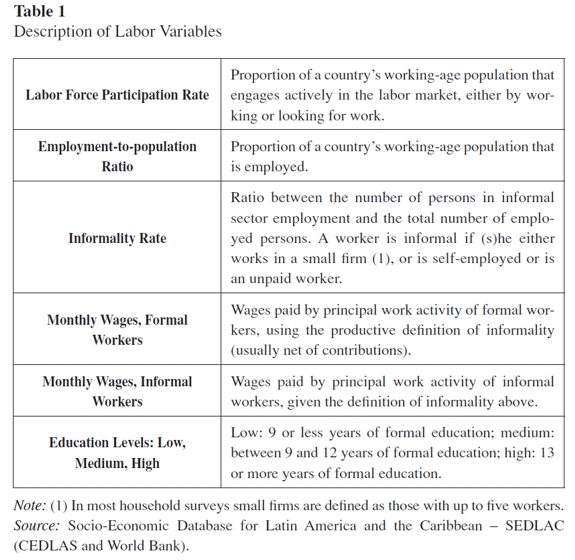

The information on all the labor variables comes from a single source, namely SEDLAC (CEDLAS and the World Bank, 2011), based on about 200 household surveys for 15 countries between 1990 and 2009. The advantage of this source is that all the variables were computed using identical methodologies, thus ensuring internal consistency and minimizing measurement errors. The main labor variables are defined in Table 18.

To assess the influence of taxation policies on labor outcomes, we focus on statutory tax rates rather than tax revenues or tax productivity variables, since the last two are more susceptible to be endogenous to the labor outcomes. The set of tax variables of interest in our analysis are payroll taxes, VAT, and corporate income taxes. Personal income taxes were excluded from the analysis because the tax rates applicable to the income levels of the large majority of workers in our samples are nil or extremely low, and display very little variation through time. Considering the extensive knowledge on the effects of import tariffs9, they have also been excluded from the analysis (although average effective tariff rates are included as controls in our regressions below).

Two control variables included in all the regressions are the GDP per capita (PPP terms, in logs) and the terms of trade (in logs). In addition, we have econometric specifications including the Kaufmann index of government effectiveness (Kaufmann, Kraay & Mastruzzi, 2009), the statutory minimum wage and a labor flexibility index (Lora, 2012). These variables measure dimensions of institutions that may change the effects of taxes on the labor market.

Finally, six other variables are included for robustness checks, all of which come from the World Development Indicators of the World Bank: (1) Population ages 25-54 (% of total WAP) and population ages 55-64 (% of total WAP), included jointly; (2) the USA real interest rate; (3) world GDP growth; (4) real effective exchange rate; (5) country's GDP growth; and (6) country's GDP terms of trade growth.

ECONOMETRIC STRATEGY

The econometric strategy attempts to exploit the (within country) variation of statutory tax rates over time in an (unbalanced) panel of 15 countries containing nearly 200 annual observations for a set of labor outcome variables during the period 1990-200910.

To explore how the set of tax variables Tit (i.e. the statutory rates of payroll, valueadded and corporate income taxes) is related with the set of labor variables Yit listed in Table 1, which are our dependent variables (for country i and period t), we initially estimate the following basic model:

| [1] |

where Xit is a set of control variables (log of GDP per capita and log of terms on trade), ti are country fixed effects and eit is the set of errors. The explanatory variables are lagged one period in order to mitigate potential endogeneity and to allow for slow adjustment processes of the dependent variables in response to changes in the regressors. The short span of our time series precludes the exploration of more complex dynamic structures. However, given the infrequent changes across time in the explanatory variables of interest (Tit), this implies little cost in terms of not adequately exploiting the dynamics of the dependent variables. The use of country fixed effects is dictated by our interest in assessing the effects on labor outcomes of changes in tax rates within countries across time, controlling for unobserved variables that might be correlated with the tax variables11.

Since institutional differences across countries in a set of dimensions Zit (which also vary over time) are important sources of heterogeneity in our analysis, the previous basic model will be expanded in the following form:

| [2] |

The additional explanatory factors attempt to capture not just the direct effect of a number of institutional features on labor outcomes but, more importantly, how those features alter the response of such outcomes to the different taxes under analysis.

In addition, we estimate several models to check for robustness of both (1) and (2). We consider the set of seven additional explanatory variables (Wit) mentioned in the last paragraph of the previous section. We estimate separate models for each additional control, which means we have six different robustness checks for the model of each dependent variable Yit with and without including the interaction of taxes with institutional variables. (Given the correlations between some of the additional control variables we have not performed combinations of several controls.) Therefore, we have two additional specifications:

| [3] |

and

| [4] |

A matter of terminology: We will consider as "strongly robust" any coefficient that is significant at least at the 5% level in at least five of the six alternative robustness tests; "mildly robust" any that is significant in three or four of the six tests; and "not robust" those that do not meet the previous criteria.

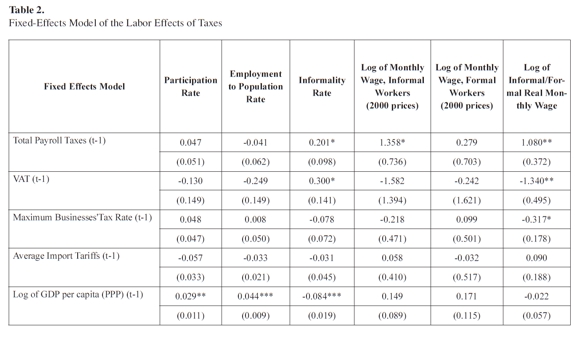

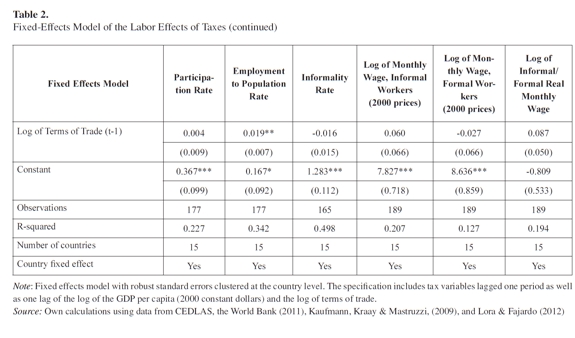

The fixed-effect estimation results of the basic model in equation (1) can be seen in Table 2, but the detailed explanation of effects below is based on results shown in Tables 4 through 8—using (2) and alternative versions of (3) and (4) above—which show the relevant coefficients for the independent variables of interest only, not the control variables or further tests or statistics. In other words, each coefficient in Tables 4 through 8 comes from a separate regression, and the number of -/+ signs indicate the degree of robustness of the coefficient, taking into account the six additional regressions per coefficient (not shown). The only general message to take from Table 2 is that most of the labor outcomes of interest do not appear to be significantly correlated with the taxes considered. As the remainder of this paper will show, this reflects the fact that the effect of any tax on the labor market may differ by skill level and may be mediated by factors such as government effectiveness, the rigidity of the labor code, and the minimum wage level.

THE LABOR EFFECTS OF PAYROLL TAXES

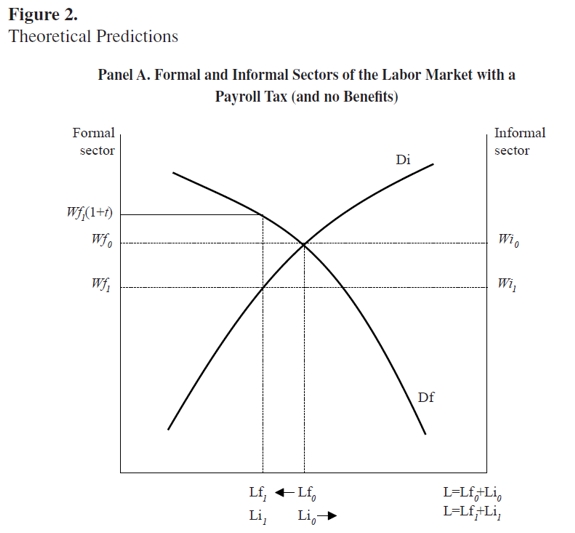

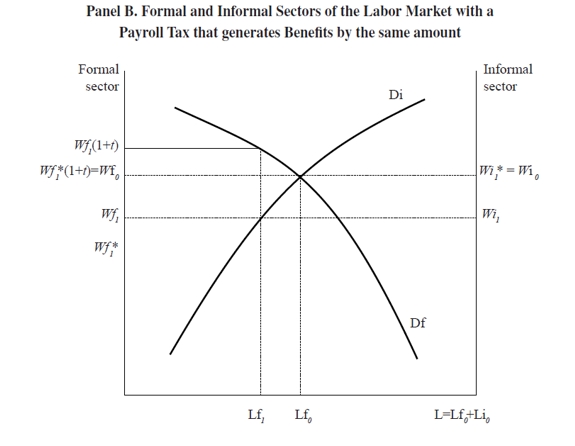

As discussed, theoretical models predict that the labor effects of payroll taxes depend on whether workers value the benefits associated with those taxes. Panel A in Figure 2 represents the case where there are no benefits, wages are fully flexible, and the labor supply is fixed. The tax introduces a wedge (t) between the cost paid by the firm and the net wage received by the workers. As a result, formal employment falls to Lf1 and net wages received by workers are reduced to wf1 in the formal segment and wi1 in the informal segment, so that all the labor force is occupied (L=Lf0+Li0). Thus, this simple framework predicts that a payroll tax that offers no individual benefits to workers increases informality and reduces wages across both sectors. If net wages in the formal segment face downward rigidity, the relative wages of the informal workers would fall. On the other hand, a payroll tax that generates benefits valued by the workers by exactly the same amount as the tax would leave the original labor market equilibrium unchanged, because the tax would be considered by workers as part of their income (Panel B, Figure 2). In this case, however, the relative wages of the informal workers would increase (by the amount of the tax) with respect to the net wages of the formal workers. Table 3 summarizes the theoretical predictions based on this analytical framework, including other possible cases that require no additional explanation.

A summary of regression results testing these hypotheses is presented in Table 4. In the base model informality increases, wages of informal workers go up and relative wages of informal workers increase, but only the final effect is robust across specifications12. This set of results may be consistent with the case where the value of benefits is less than or equal to the tax and there are no wage rigidities. However, in that case the analytical framework predicts that net wages, both in the formal and the informal segments should fall, which is not observed. The results by educational group are even weaker. Only in the case of medium-education workers do the relative wages of informal workers increase, but informality does not increase and wages do not fall.

Apparently, therefore, payroll taxes do not have clear effects on labor markets. This, however, is the result of mixing different types of payroll taxes within the bag of total payroll taxes.

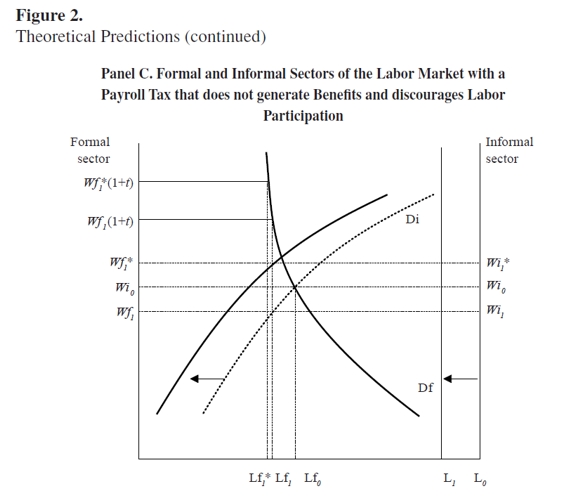

A simple distinction to be made is between contributions that entitle workers (and in some countries their families also) to health services, and other payroll taxes13. Presumably, contributions to health social security may be valued by the average worker more highly than other services usually financed by other payroll taxes, such as pensions, labor training, subsidized housing, and childcare and recreation services, which give access to benefits in a distant future (pensions) or benefit only some workers, and oftentimes benefit those not working (see Levy, 2008, for the case of Mexico). Furthermore, contributions entitling workers to benefits that are highly valued by certain groups of workers may encourage labor participation by reducing the reservation wage of those workers. In a similar way, contributions that finance social services to those not in the labor market may discourage labor participation. For convenience, we present the latter case first.

Consider Panel C, Figure 2, which represents the effects of payroll taxes that offer no benefits to those contributing and discourage labor participation. Before the tax, equilibrium in the labor market is achieved when wages in the formal and informal segments are equal at level wf0= wi0. If the labor supply were fixed, the new net wage levels would be lower, at wf1= wi1, and gross wages in the formal sector would be wf1(1+t), where t is the tax. However, the supply of labor may contract if the payroll tax finances social services that raise the reservation wage of some workers. In the figure this implies a shift to the left of total labor supply L, and a corresponding shift in the demand for labor in the informal sector (since it is drawn from right to left). This will increase wages with respect to the level wf1= wi1. Depending on the elasticity of the demand for labor in the formal segment, the final wage levels (wf1*= wi1*) may be even higher than wf0= wi0, as shown in the figure. Informality rates may increase or fall, depending on the elasticities. If, in addition to the changes presented in the figure, the tax generates some (partial) benefits to formal workers, the relative wages of informal workers will increase.

The empirical results presented in Table 4 for "other payroll taxes" (other than health social security contributions) are consistent with the predictions of this analytical framework when the taxes discourage labor participation, some partial benefits are provided to formal workers, and labor demand in the formal segment of the economy is inelastic. The fall of the employment rate is statistically significant and robust (0.136 for each point of increase in payroll taxes in the basic specification). Also statistically significant and robust are the increase in net real wages (2.1%) and the increase in the relative wages of informal workers (1.8%).

Similar results hold for the group of workers with low education14. In the mediumeducation groups no discouragement effect is observed, but wages still go up, suggesting strong labor demand substitutability with the low-education group. In the high-education group, higher payroll taxes encourage labor supply and increase wages evenly in the formal and the informal segments, though less than in the low education group (also suggesting high labor demand substitutability), and further implying that this type of worker does not value the benefits they may receive.

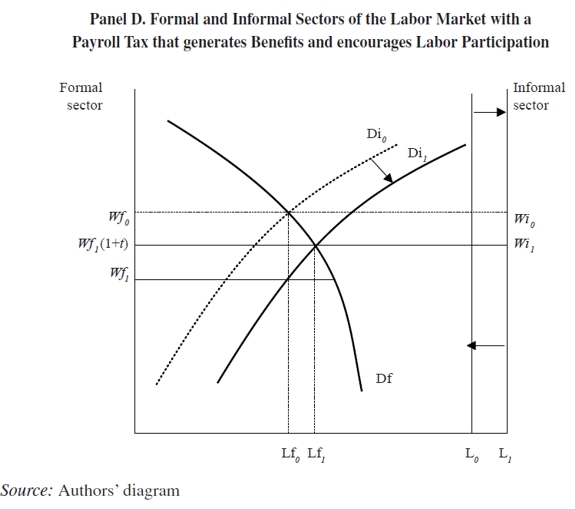

Consider next a payroll tax that entitles workers to benefits and encourages labor supply. As described in Panel D, Figure 2, workers in both the formal and the informal segments will receive lower wages because of the increase in labor supply, but wages of informal workers relative to those of formal workers will rise because the latter will consider the benefits part of their remuneration. Both formal and informal employment will increase, and therefore the informality rate may go either way.

Table 4, Health, all groups). In some specifications informality is increased, but the result is not robust. This is consistent with the hypothesis that, unlike other payroll taxes, the benefits of health social security contributions are highly valued, especially by marginal workers. Indeed, the labor supply response and the reduction in wages are stronger among low- and medium-education groups.

This description partially fits the econometric results in the case of health social security contributions. They encourage labor participation and reduce wages across the board. Both results are robust, with estimated coefficients of 0.4 and -1.3, respectively (see Labor participation among high-education groups is not affected but net wages do fall, implying that these workers do value health social security services. However, the econometric results do not support the theoretical prediction on the relative wages of informal workers. The fact that their relative wages do not increase for any of the education groups (and do increase significantly for all groups combined) seems to imply that workers in small firms (our definition of informality) are not excluded from health services, either because they do contribute or have subsidized access to health services.

Whether higher payroll taxes do increase labor costs, especially in smaller firms, may depend on tax enforcement capabilities and other factors that influence tax compliance and tax morale. In order to test the hypothesis that better tax enforcement capabilities may affect the labor effects of payroll taxes, an interaction term (payroll taxes X government effectiveness) is introduced in the basic regression (see Table 4), where government effectiveness is taken as a proxy of those capabilities. As expected, the results indicate that stronger capabilities reinforce the influence of payroll taxes on the wages of informal workers, a result that is strongly robust across specifications. However, no significant changes are observed in other labor variables.

Theory and previous empirical studies for developed countries indicate that wage rigidities and labor market institutions in general may alter the influence of payroll taxes on labor outcomes. In order to test the hypothesis we expand our basic estimates to include interaction terms of payroll taxes with the relative level of minimum wages (with respect to average wages) and with an index of labor market flexibility (Lora, 2012).

Minimum wages do not seem to have any significant influence on the labor effects of payroll taxes (the conclusion is valid for each of the three education groups). This does not completely rule out the hypothesis, however, because the variable measuring minimum wages does not capture the degree of compliance.

The flexibility of labor market institutions does have an important influence on the impact of payroll taxes. Since more flexible labor markets facilitate hiring and firing workers (and faster wage adjustments through labor churning), they should be expected to reinforce the effects of payroll taxes on participation, employment, and wages, as is indeed found. The coefficients of this interaction term (payroll taxes X labor reform index) are highly significant and strongly robust in the regressions of those dependent variables. This also holds for the low- and medium-education groups, though not for the high-education group.

In summary, the effects of payroll taxes on the labor market depend strongly on the type of tax, and to some extent on the level of education of the workers and the flexibility of labor market institutions. Payroll taxes have more deleterious effects on the labor market when their contributions are not valued by workers, but such valuation seems to be heterogeneous across education groups. Effects are stronger when labor markets are more flexible.

THE LABOR EFFECTS OF VAT

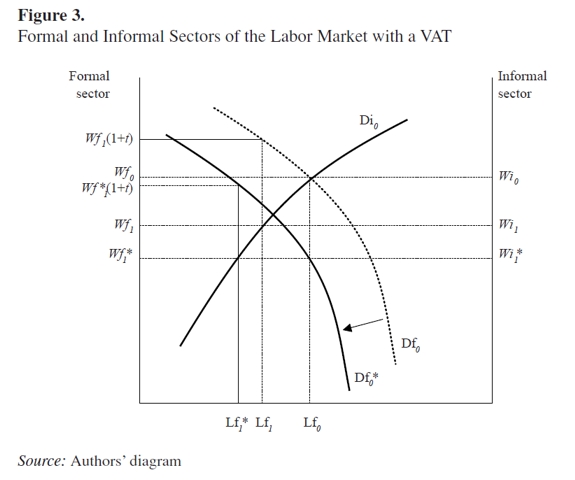

The main difference between a payroll tax (not tied to benefits for the workers paying it) and a flat VAT is that the former is levied on the valued added by labor only, while the latter is levied both on labor and capital earnings. In the presence of informality, a VAT will induce more informality and lower wages than a payroll tax levied at the same rate, as shown in Figure 3. As a VAT is levied on profits also, it reduces formal labor demand, because the resulting fall in the stock of capital in the formal segment reduces labor productivity. In the figure we assume that nothing happens with labor demand in the informal sector, which is a simplification. Labor productivity in the informal sector may increase if capital moves to the sector, attracted by the cost advantage that a VAT implicitly gives to the smaller firms, which have a better chance of going undetected if they do not pay taxes. On the other hand, since informal firms buy at least some of their inputs from formal firms, more expensive inputs may impair labor productivity. As shown in the figure, compared with a payroll tax at the same rate, a VAT produces a larger decline in wages and more informality (given total labor supply). The first row of Table 5 summarizes the hypotheses so far.

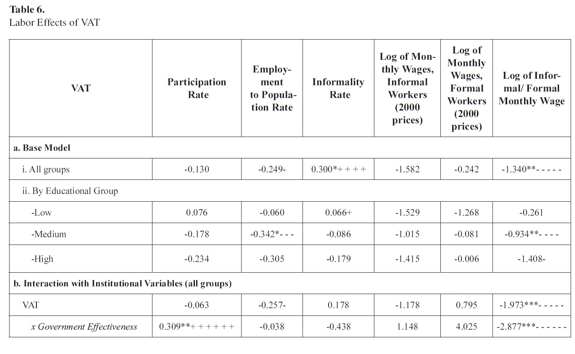

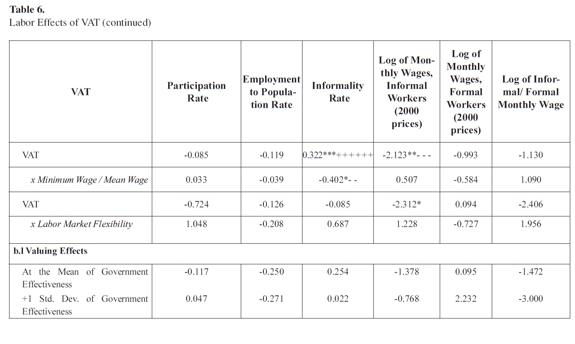

The econometric results in Table 6 confirm the effect on informality (which is mildly robust): A one percentage point increase in the VAT raises the informality rate by 0.3 percentage points. The results indicate that relative wages of informal workers fall significantly, which suggests that formal wages may face some downward rigidity, as discussed below.

The increase of informality is largely due to changes in the composition of labor, as employment rates fall for the medium- and high-education groups, which have lower informality rates. The fall in the relative wages of the informal workers is less affected by the compositional changes mentioned: Most of the effect is caused by a reduction in the relative remuneration of informal workers in each education group, especially in the medium-education group.

The differential effects of the VAT by education groups may be due to different degrees of substitutability between capital and low- and high-skills groups. If capital is a substitute for unskilled labor but a complement to skilled labor, the demand for the former will fall less than that for the latter. In Figure 3, this would imply that the demand for labor in the formal sector is shifted less to the left in the case of unskilled labor; under some assumptions about the elasticities of substitution, it may even shift to the right. If, in addition, there is some type of wage rigidity that impedes a wage decline in the formal segment, wages in the informal segment will fall with respect to those in the formal segment among skilled workers. The last rows of Table 4 summarize the hypotheses for the low- and high-skills groups.

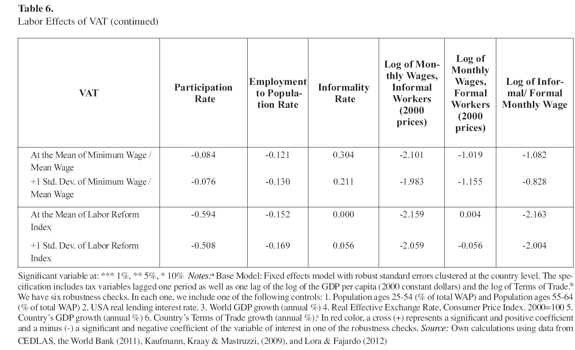

Indeed, the remunerations of high-education workers are not immune to changes in VAT rates15. Although there is much heterogeneity across countries, in a country with a level of minimum wages equivalent to the average for the region, a one percentage point increase in the VAT basic rate is associated with a decline of 3.1 percentage points in the absolute level of wages of informal workers, and a 0.7 point increase in those of formal workers. In contrast, in a country where the minimum wage is one standard deviation higher, the wages of informal workers fall 4.4 percentage points for each point of increase in the VAT, and those of the formal workers remain the same.

Heterogeneity in tax enforcement capabilities (proxied here by the variable government effectiveness) may also alter the impact of the VAT. When capabilities are stronger, an increase in the VAT rate is associated with higher unemployment rates among the low-education groups (the effect is only mildly robust). Value-added taxes are often considered less distortive than other taxes because they affect all sectors and factors in a more homogeneous way than other taxes.

However, our results suggest that, in the presence of informality, the effects of the VAT on production and investment decisions may be less innocuous than usually assumed. Increases in VAT rates are associated with higher informality rates and with steep reductions in the relative wages of informal workers. The effects differ greatly by education groups, and these differences may be increased by institutional features of the labor market, especially by wage rigidities. If capital is a substitute for unskilled labor but a complement to skilled labor, the impact of the VAT should be stronger for the latter, as our results indicate.

The effects of the corporate income tax, to which we now turn, will also suggest that differential effects by education level may be due to the fact that capital is a substitute for unskilled labor but a complement to skilled labor.

THE LABOR EFFECTS OF CORPORATE INCOME TAXES

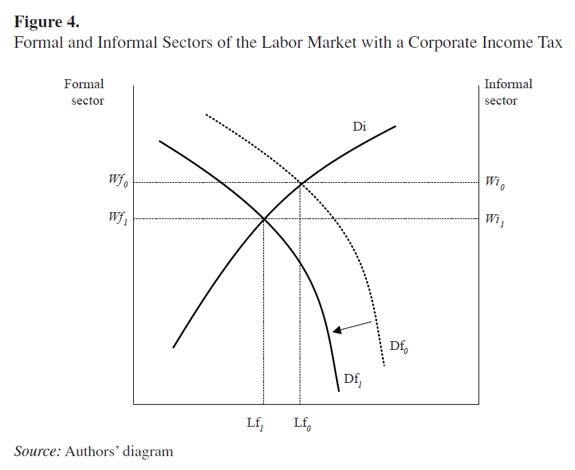

A corporate income tax that is paid by formal firms will only reduce labor productivity in those firms because investment and the stock of capital in those firms will fall. As shown in Figure 4, this will shift formal labor demand to the left, leading to a decline in wages and an increase in informality.

The changes in wages and informality that are needed to restore equilibrium will depend on the elasticities of the labor demand curves. The more inelastic the curves, the larger the changes in wages needed to restore equilibrium (but the smaller the change in informality).

However, at least four additional effects may modify these basic results. First, with several skill levels, the size and even the direction of change of their specific labor market outcomes may differ from the general result. If skilled labor is a complement to capital but unskilled labor is a substitute, skilled formal labor demand will shift further to the left than unskilled labor demand, implying that the relative wages of the skilled will fall with respect to the unskilled, and that informality of the former will increase more than that of the latter. Under certain assumptions, informality rates of the unskilled may fall, as shown by Ahmad and Best (2012).

Second, some capital may move from the formal to the informal sector, attracted by the possibility of evading the tax, which will shift informal labor demand to the left (since it is drawn from right to left), reinforcing the increase in informality but attenuating the decline of wages. Since the ability of capital to escape the purview of the tax administration and move to the informal sector will depend on tax enforcement capabilities, the stronger the capabilities, the smaller the increase in informality. If skilled labor and capital are complements, the stronger the capabilities, the worse the impact of the tax on wages and employment of skilled workers.

Third, if there are downward wage rigidities in the formal segment of the labor market due, for instance, to a binding minimum wage, relative wages of informal workers will fall with respect to those in the formal segment if corporate income taxes increase informality. The extent to which a higher corporate income tax rate affects informality and wages may also depend on the degree of flexibility of the labor code. If labor mobility between the formal and the informal segment is facilitated by institutional factors such as a flexible labor code, increases in corporate income tax will lead to reallocation of labor between the formal and the informal segment, producing larger increases in informality but smaller reductions in wages (especially for informal workers, if there is some wage rigidity in the formal segment).

Fourth, labor supply may react as wages and labor opportunities change. In particular, skilled labor supply may fall, especially if informal employment opportunities are limited. Labor supply changes will weaken the effect of the tax on relative wages and informality.

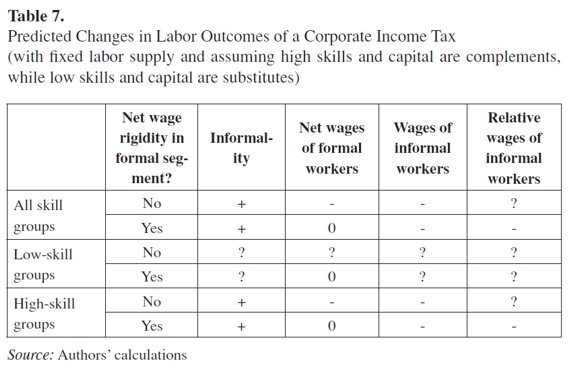

Table 7 summarizes the main theoretical predictions when capital and high skills are complements (and capital and low skills are substitutes), assuming that labor supply is fixed, and ignoring the influence of government tax enforcement capabilities and labor code rigidities (other than a minimum wage).

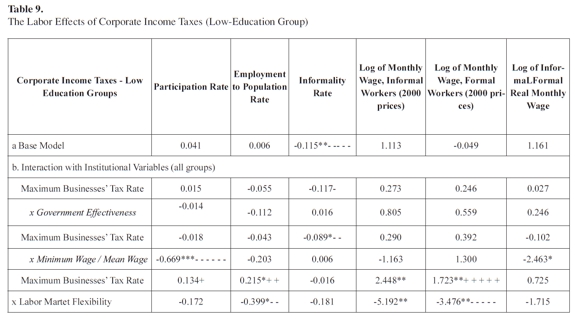

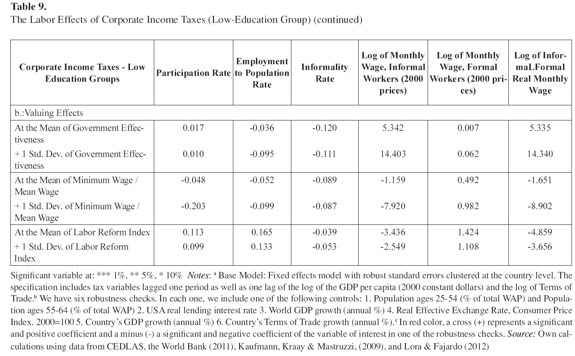

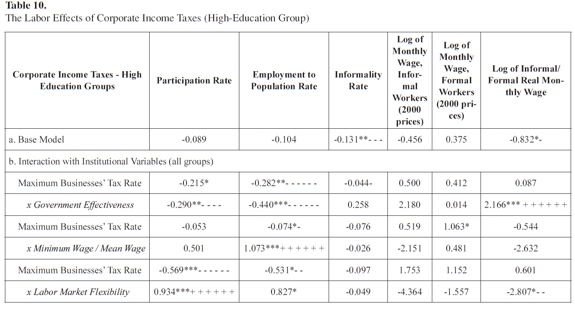

The maximum rate is the only observable dimension of corporate income tax regimes for which we have enough data to test the predictions. Since the effects may depend on several institutional factors and on the degree of substitutability between capital and the different types of labor, it is not surprising that none of the aggregate labor variables considered has a statistically significant relation with the maximum corporate income tax rate (see base model, all groups in Table 8). However, some important effects become apparent when splitting the sample by education levels and when taking into consideration the heterogeneity resulting from institutional factors.

Corporate income taxes do affect workers with different skills in different ways. Low-education workers tend to do better, as reflected in higher wages—especially in the informal segment—and lower informality rates. In contrast, high- and mediumeducation workers tend to become worse off. Those in the informal segment see their relative wages fall, and while informality rates go down, especially among the higheducation group, participation and employment falls. While some of these effects are not significant in the base models by educational groups presented in Tables 9 and 10, they become more pronounced when institutional factors are brought into the picture.

For low-education groups (Table 9), higher corporate income tax rates are associated with statistically significant reductions in informality (independent of other institutional factors). When the heterogeneity in labor market flexibility is controlled for, higher corporate income taxes are also associated with higher wages (overall and in the formal segment). In more flexible labor markets, wage increases are somewhat smaller than in less flexible ones. However, the ability of the government to enforce the tax regime does not seem to alter the labor opportunities of this group of workers.

In contrast, for high-education groups (Table 10), higher government effectiveness is associated with a significant impact of corporate income taxes on occupation and on the relative wages of informal workers. In a country where government effectiveness is at the average level of the region, an increase in the corporate income tax rate is associated with changes of these variables that are much smaller (and even of the opposite sign, in the case of relative wages) than in a country where government effectiveness is one standard deviation higher. Consider the discouraging effect on high-education workers: In a country where government effectiveness is equal to the average in the region, an increase of 10 points in the corporate tax rate reduces the employment rate of the highly skilled by 2 percentage points, while in a country where government effectiveness is one standard deviation higher, the same increase in corporate income tax reduces the employment rate of the highly skilled by 4.4 percentage points. In the former country the wages of the skilled workers operating independently or in small firms fall slightly with respect to their peers in larger firms, while in the latter country their wages increase 13%, or 8% more than those of their peers, reflecting the decline in supply and the higher operating costs for those remaining in the informal segment. The reduction in the informality rate of the higheducation workers when the corporate income tax rate goes down— a result that is mildly robust statistically and which seems an anomaly in view of our analytical framework— is probably a result of the discouragement effect.

CONCLUSION

Knowledge about the effects that taxes produce on labor outcomes in Latin American economies is very scant. This paper is an attempt to fill this vacuum. Using national-level data on labor variables for 15 Latin American countries, it has empirically explored the effects of payroll taxes, value-added taxes and corporate income taxes on labor participation, employment, informality, and wages.

Three main general conclusions emerge from this paper. First, the results indicate that each tax produces different effects, as should be expected on the basis of previous theoretical and empirical work, mostly for developed countries. Second, the results uncover the importance of several aspects of labor and tax institutions that are specific to developing countries, especially those associated with the presence of informality, such as the weak enforcement of tax and labor codes. And third, the empirical findings lend strong support to the hypothesis that the labor effects of taxes differ markedly across skill groups.

More specifically, this paper contributes to understanding the effects of each tax. In the case of payroll taxes, the labor impacts differ strongly by type of tax, with those not valued by workers inducing the greatest increases of labor costs and losses of employment, in contrast with those more valued by workers, which increase labor participation and do not raise labor costs for firms.

Value-added taxes are often assumed to generate more homogeneous effects on all sectors and factors than other, supposedly more distortive taxes. However, our results indicate that the presence of informality renders these assumptions invalid. Since a VAT makes informal activities more competitive vis-à-vis their formal competitors, but informal activities are less skill-intensive than formal ones, skilled workers tend to be more affected than unskilled ones.

Corporate income taxes also affect skilled workers more than unskilled workers because of the complementarity between capital and skilled labor. However, unlike VAT, corporate income taxes encourage unskilled workers to move from the informal to the formal segment of the economy, where they become more attractive as a substitute to capital. At the same time, and also unlike VAT, higher corporate income taxes are associated with lower labor participation and employment of high-education workers, especially in countries where tax enforcement capabilities are stronger.

These findings open new avenues for further research. From a theoretical perspective, they provide important stylized facts that should be taken into consideration in general equilibrium models aimed at understanding the effects of taxes in developing economies. In particular, the separation of the labor market by skills and the inclusion of an informal segment should be considered essential elements of such models. From an empirical point of view, much work remains to be done to test the validity of the findings and the interpretations we have provided.

Our database is too aggregated and our measures of taxes too crude to provide final answers to the effects of tax reforms that are always more nuanced than just a change in the basic tax rate. By exploiting the different treatment of sectors and goods in most tax reforms, future empirical work could provide more robust findings on their effects on employment and wages (in a way similar to the abundant research on the labor effects of import tariff reductions in the 1990s in Latin America). Our findings should also encourage empirical research into the effects of taxes on labor income inequality. Most analyses on tax incidence rely on extremely crude incidence assumptions and totally disregard the effects that taxes have on wages and employment. Since, as we have shown, those effects can be quite large and are not homogeneous across educations groups, taxes may have more important distributional effects through the labor market than directly on disposable real incomes.

FOOTNOTES

1 For further information on these figures and sources of data, see the Data Sources section.

2 This subsection draws heavily from Kugler (2011).

3 For a complete list of references see the working paper version of this paper (Lora & Fajardo, 2012).

4 For a survey of the (mainly theoretical) general equilibrium models used to assess effects of VAT on informality, see the working paper version of this article (Lora & Fajardo, 2012).

5 For a survey of the (mainly theoretical) general equilibrium models used to assess effects of VAT on informality, see the working paper version of this article (Lora & Fajardo, 2012).

6 Enforcement efforts may affect the transmission of evasion of VAT, as found through a randomized experiment among Chilean firms by Pomeranz (2013).

7 For the former see Carroll et al. (2000) and Bettendorf, van der Horst & De Mooij (2009).

8 In the working paper version of this article we provided basic statistical indicators of the variables in Table 1, as well as of the tax variables (Lora & Fajardo, 2012).

9 Lora (2011) surveys the vast empirical literature on the subject.

10 The longest available when the research was done.

11 We conducted panel unit root tests to test for stationarity. All of our dependent variables are stationary according to the results obtained using a Fisher-type test that does not require strongly balanced data, like ours. All the independent variables are also stationary, with the exception of GDP. However, we have also included GDP growth as a control.

12 As mentioned before, robustness checks are performed introducing seven controls, one by one, except for the population shares. The number of positive or negative signs in the summary tables corresponds to the number of those checks where the coefficient is significant at least at the 95% confidence level. Complete regression results can be found in the working paper version of this article.

13 Another possibility is to distinguish between social security contributions (including health and pensions) and other payroll taxes. With such a distinction, the results presented below are basically the same, though somewhat weaker. More complex distinctions, though justifiable in theory, cannot be implemented with our database, given the limited number of changes in the relevant contribution rates.

14 See the working paper version of this paper for detailed results by education level.

15 For detailed results by education level see Lora & Fajardo (2012).

REFERENCES

[1] Ahmad, E., & Best, M. (2012). Design and financing of social programs in the presence of informality. Paper presented at the Inter-American Development Bank, Washington, DC

[2] Bettendorf, L., Van der Horst, A., & De Mooij, R. A. (2009). Corporate tax policy and unemployment in Europe: An applied general equilibrium analysis. World Economy, 32(9), 1319-47.

[3] Bird, R. M., & Gendron, P. P. (2007). The VAT in developing and transitional countries. New York, NY: Cambridge University Press.

[4] Carroll, R., Holtz-Eakin, D., Rider, M., & Rosen, H. S. (2000). Income taxes and entrepreneurs' use of labor. Journal of Labor Economics, 18(2), 324-51.

[5] Centro de Estudios Distributivos Laborales y Sociales (CEDLAS) and World Bank. (2011). Socio-Economic Database for Latin America and the Caribbean (SEDLAC). Available at: http://sedlac.econo.unlp.edu.ar/eng/.

[6] Cerda, R. A., & Larraín, F. (2010). Corporate taxes and the demand for labor and capital in developing countries. Small Business Economics, 34(2), 187-201.

[7] Cox Edwards, A. (2002). Payroll taxes (Working Paper 132). Stanford, CA: Stanford University, Center for Research on Economic Development and Policy Reform.

[8] Cruces, G., Galiani, S., & Kidyba, S. (2010). Payroll taxes, wages and employment: Identification through Policy Changes. Labour Economics, 17, 743-49.

[9] De Paula, á., & Scheinkman, J. A. (2010). Value-Added Taxes, Chain effects, and informality. American Economic Journal: Macroeconomics, 2(4), 195-221.

[10] Friedman, E., Johnson, S., Kaufmann, D., & Zoido-Lobaton, P. (2000) Dodging the grabbing hand: The determinants of unofficial activity in 69 countries. Journal of Public Economics, 76(3), 459-93.

[11] Gruber, J. (1997). The incidence of payroll taxation: Evidence from Chile. Journal of Labor Economics, 15(3), S72-S101.

[12] Heckman, J., & Pagés C., editors. (2004). Law and employment: Lessons from Latin America and the Caribbean. Chicago, IL: University of Chicago Press.

[13] Johnson, S., Kaufmann, D., & Shleifer, A. (1997). The unofficial economy in transition. Brookings Papers on Economic Activity, 2, 159-239.

[14] Kaufmann, D., Kraay A., & Mastruzzi, M. (2009). Governance matters VIII: Aggregate and individual governance indicators 1996-2008 (Policy Research Working Paper 4978). Washington, DC: World Bank.

[15] Keen, M., & Lockwood, B. (2010). The value added tax: Its causes and consequences. Journal of Development Economics, 92(2), 138-51.

[16] Kugler, A. (2011). Is there an anti-labor bias of Taxes? A survey of the evidence from Latin America and around the World (Technical Notes IDBTN- 299). Washington, DC: Inter-American Development Bank.

[17] Kugler, A., & Kugler, M. (2009). Labor market effects of payroll taxes in developing countries: Evidence from Colombia. Economic Development and Cultural Change, 57(2), 335-58.

[18] Levy, S. (2008). Good intentions, bad outcomes: Social policy, informality, and economic growth in Mexico. Washington, DC: Brookings Institution Press.

[19] Loayza, N. V. (1996). The economics of the informal sector: A simple model and some empirical evidence from Latin America. Carnegie- Rochester Conference Series on Public Policy, 45, 129-62.

[20] Lora, E. (2011). The effects of trade liberalization on growth, employment, and wages. In: J. A. Ocampo and J. Ros (Eds.), The Oxford Handbook of Latin American Economies. Oxford: Oxford University Press, 368-393

[21] Lora, E. (2012). Structural reforms in Latin America: What has been reformed and how it can be quantified (updated version) (Research Department Working Paper 4809). Washington, DC: Inter-American Development Bank.

[22] Lora, E., & Fajardo, J. (2012). Employment and taxes in Latin America: An empirical study of the effects of payroll, corporate and value-added taxes on labor outcomes (Research Department Working Paper 4791). Washington, DC: Inter-American Development Bank.

[23] Martínez, C., Morales, G., & Valdés R. (2001). Cambios estructurales en la demanda por trabajo en Chile. Economía Chilena, 4(2), 5-25.

[24] Melguizo, á. (2009). ¿Quién soporta las cotizaciones sociales empresariales y la fiscalidad laboral? Una panorámica de la literatura empírica. Hacienda Pública Española / Revista de Economía Pública, 188(1), 125-182.

[25] OECD. (2011). Taxation and employment (Tax Policy Studies 21). Paris: Organization for Economic Co-operation and Development.

[26]. Pomeranz, D. (2013). No taxation without information: Deterrence and self-enforcement in the value added tax. National Bureau of Economic Research, Working Paper No. 19199

[27] Slemrod, J. (2008). Does it matter who writes the check to the government? The economics of tax remittance. National Tax Journal, 61(2),251-75.

[28] Vuletin, G. (2008). Measuring the informal economy in Latin America and the Caribbean (IMF Working Paper 102). Washington, DC: International Monetary Fund.

Referencias

Ahmad, E., & Best, M. (2012). Design and financing of social programs in the presence of informality. Paper presented at the Inter-American Development Bank, Washington, DC

Bettendorf, L., Van der Horst, A., & De Mooij, R. A. (2009). Corporate tax policy and unemployment in Europe: An applied general equilibrium analysis. World Economy, 32(9), 1319-47.

Bird, R. M., & Gendron, P. P. (2007). The VAT in developing and transitional countries. New York, NY: Cambridge University Press.

Carroll, R., Holtz-Eakin, D., Rider, M., & Rosen, H. S. (2000). Income taxes and entrepreneurs' use of labor. Journal of Labor Economics, 18(2), 324-51.

Centro de Estudios Distributivos Laborales y Sociales (CEDLAS) and World Bank. (2011). Socio-Economic Database for Latin America and the Caribbean (SEDLAC). Available at: http://sedlac.econo.unlp.edu.ar/eng/.

Cerda, R. A., & Larraín, F. (2010). Corporate taxes and the demand for labor and capital in developing countries. Small Business Economics, 34(2), 187-201.

Cox Edwards, A. (2002). Payroll taxes (Working Paper 132). Stanford, CA: Stanford University, Center for Research on Economic Development and Policy Reform.

Cruces, G., Galiani, S., & Kidyba, S. (2010). Payroll taxes, wages and employment: Identification through Policy Changes. Labour Economics, 17, 743-49.

De Paula, á., & Scheinkman, J. A. (2010). Value-Added Taxes, Chain effects, and informality. American Economic Journal: Macroeconomics, 2(4), 195-221.

Friedman, E., Johnson, S., Kaufmann, D., & Zoido-Lobaton, P. (2000) Dodging the grabbing hand: The determinants of unofficial activity in 69 countries. Journal of Public Economics, 76(3), 459-93.

Gruber, J. (1997). The incidence of payroll taxation: Evidence from Chile. Journal of Labor Economics, 15(3), S72-S101.

Heckman, J., & Pagés C., editors. (2004). Law and employment: Lessons from Latin America and the Caribbean. Chicago, IL: University of Chicago Press.

Johnson, S., Kaufmann, D., & Shleifer, A. (1997). The unofficial economy in transition. Brookings Papers on Economic Activity, 2, 159-239.

Kaufmann, D., Kraay A., & Mastruzzi, M. (2009). Governance matters VIII: Aggregate and individual governance indicators 1996-2008 (Policy Research Working Paper 4978). Washington, DC: World Bank.

Keen, M., & Lockwood, B. (2010). The value added tax: Its causes and consequences. Journal of Development Economics, 92(2), 138-51.

Kugler, A. (2011). Is there an anti-labor bias of Taxes? A survey of the evidence from Latin America and around the World (Technical Notes IDBTN- 299). Washington, DC: Inter-American Development Bank.

Kugler, A., & Kugler, M. (2009). Labor market effects of payroll taxes in developing countries: Evidence from Colombia. Economic Development and Cultural Change, 57(2), 335-58.

Levy, S. (2008). Good intentions, bad outcomes: Social policy, informality, and economic growth in Mexico. Washington, DC: Brookings Institution Press.

Loayza, N. V. (1996). The economics of the informal sector: A simple model and some empirical evidence from Latin America. Carnegie- Rochester Conference Series on Public Policy, 45, 129-62.

Lora, E. (2011). The effects of trade liberalization on growth, employment, and wages. In: J. A. Ocampo and J. Ros (Eds.), The Oxford Handbook of Latin American Economies. Oxford: Oxford University Press, 368-393

Lora, E. (2012). Structural reforms in Latin America: What has been reformed and how it can be quantified (updated version) (Research Department Working Paper 4809). Washington, DC: Inter-American Development Bank.

Lora, E., & Fajardo, J. (2012). Employment and taxes in Latin America: An empirical study of the effects of payroll, corporate and value-added taxes on labor outcomes (Research Department Working Paper 4791). Washington, DC: Inter-American Development Bank.

Martínez, C., Morales, G., & Valdés R. (2001). Cambios estructurales en la demanda por trabajo en Chile. Economía Chilena, 4(2), 5-25.

Melguizo, á. (2009). ¿Quién soporta las cotizaciones sociales empresariales y la fiscalidad laboral? Una panorámica de la literatura empírica. Hacienda Pública Española / Revista de Economía Pública, 188(1), 125-182.

OECD. (2011). Taxation and employment (Tax Policy Studies 21). Paris: Organization for Economic Co-operation and Development.

. Pomeranz, D. (2013). No taxation without information: Deterrence and self-enforcement in the value added tax. National Bureau of Economic Research, Working Paper No. 19199

Slemrod, J. (2008). Does it matter who writes the check to the government? The economics of tax remittance. National Tax Journal, 61(2),251-75.

Vuletin, G. (2008). Measuring the informal economy in Latin America and the Caribbean (IMF Working Paper 102). Washington, DC: International Monetary Fund.

Cómo citar

APA

ACM

ACS

ABNT

Chicago

Harvard

IEEE

MLA

Turabian

Vancouver

Descargar cita

CrossRef Cited-by

1. Margarita Velín-Fárez. (2025). Fiscal sustainability and universal pensions: Public pensions in Ecuador. Cuadernos de Economía, 44(95) https://doi.org/10.15446/cuad.econ.v44n95.106644.

2. Shengqiang Zuo, Bangzheng Wu, Jun Feng. (2022). Does Government Reduce the Corporate Income Tax Rate Increase Employment? Evidence from China. SSRN Electronic Journal, https://doi.org/10.2139/ssrn.4102966.

3. Shengqiang Zuo, Bangzheng Wu, Jun Feng. (2023). Does government reduction of the corporate income tax rate increase employment? Evidence from China. International Review of Economics & Finance, 83, p.365. https://doi.org/10.1016/j.iref.2022.09.002.

4. Dürdane Şirin Saraçoğlu. (2020). Do labour market policies reduce the informal economy more effectively than enforcement and deterrence?. Journal of Policy Modeling, 42(3), p.679. https://doi.org/10.1016/j.jpolmod.2020.01.010.

5. Leonardo Fabio Morales-Zurita, Carlos Alberto Medina-Durango. (2016). Assessing the effect of payroll taxes on formal employment : the case of the 2012 tax reform in Colombia. https://doi.org/10.32468/be.971.

6. Alcides Palacios. (2020). Estructura y cultura socio-económica de la comunidad campesina en el Perú. Revista Innova Educación, 2(4), p.576. https://doi.org/10.35622/j.rie.2020.04.005.

7. Pablo Adrian Garlati-Bertoldi. (2020). Change at Home, in the Labor Market, and On the Job. , p.153. https://doi.org/10.1108/S0147-912120200000048005.

8. Andy McKay, Jukka Pirttilä, Caroline Schimanski. (2024). The Tax Elasticity of Formal Work in Sub-Saharan African Countries. The Journal of Development Studies, 60(2), p.217. https://doi.org/10.1080/00220388.2023.2279477.

Dimensions

PlumX

Visitas a la página del resumen del artículo

Descargas

Licencia

Derechos de autor 2016 Cuadernos de EconomíaCuadernos de Economía a través de la División de Bibliotecas de la Universidad Nacional de Colombia promueve y garantiza el acceso abierto de todos sus contenidos. Los artículos publicados por la revista se encuentran disponibles globalmente con acceso abierto y licenciados bajo los términos de Creative Commons Atribución-No_Comercial-Sin_Derivadas 4.0 Internacional (CC BY-NC-ND 4.0), lo que implica lo siguiente: