Publicado

El papel de los herederos en las empresas familiares: El caso de Carvajal

The role of heirs in family businesses: The case of Carvajal

Le rolé des héritiers dans les entreprises familiales: Le cas de Carvajal

O papel dos herdeiros nas empresas familiares: O caso de Carvajal

Palabras clave:

Empresas familiares, sucesiones, herederos como gerentes (es)Family businesses, successions, heirs as managers (en)

Entreprises familiales, successions, gérants héritiers (fr)

empresas Familiares, sucessoes, herdeiros como dirigentes (pt)

En este artículo extendemos el modelo de sucesión familiar de Patia, Ravid y Wang (2008), Y argumentamos que los gerentes familiares pueden ser exitosos si ciertos factores se presentan, como un conocimiento tácito, beneficios no monetarios al dirigir la empresa, y el desarrollo de ciertas habilidades gerenciales personales. Utilizamos un importante grupo económico colombiano para soportar nuestras ideas y mostrar que, contrario a la evidencia empírica internacional. Existen ciertas circunstancias bajo las cuales los esfuerzos que que hacen los herederos en la gerencia pueden ser similares a los del fundador y mayores a los de los gerentes externos.

Cet article considére le modéte de succession familiale de Palia, Ravid y Wang (2008), et l'argument consiste en ce que les gérants familiaux peuvent arriver au succes si certains tacteurs se présentent, tels que la connaissance tacite, les benefices non monetaires dans la direction de I'entreprise, el Ie developpement de certaintes habiletés de gestions personnelles, le cas de Carvajal est utilisé, un important groupe económique colombien, pour developper nos idées et montrer que, contrairement á l´evidence empirique internationale, il existe certaines circonstances dans lesquelles les efforts réalisés par les héritiers dans la gestion peuvent étre semblables á ceux du fondateur et supérieurs á ceux de gerants externes.

Neste artigo estendemos o modelo de sucessao familiar de Palia, Ravid y Wang (2008), e argumentamos que os dirigentes familiares podem ser bem sucedidos se certos fatores apresentam-se, como um conhecimento tácito nao monetarios ao dirigir a empresa, e o desenvolvimento de certas habilidades gerenciais pessoais. Utilizamos o caso de Carvajal, um importante grupo económico colombiano, para suportar nossas idéias e mostrar que, ao contrário da evidéncia empirica internacional, existem certas circunstancias sob as quais os esfonços que fazem os herdeiros na direçao podem ser similares aos do fundador e maiores aos dos dirigentes externos.

Maximiliano González Ferrero*, Alexánder Guzmán Vásquez**, María Andrea Trujillo Dávila***

* Associate Professor, School of Management, Universidad de los Andes, Bogotá, Colombia. E-mail: mgf@adm.uniandes.edu.co

** PhD (c), School of Management, Universidad de los Andes and Associate Professor, Colegio de Estudios Superiores de Administración - CESA, Bogotá, Colombia. E-mail: ale-guzm@uniandes.edu.co

*** PhD (c), School of Management, Universidad de los Andes and Associate Professor, Colegio de Estudios Superiores de Administración - CESA, Bogotá, Colombia. E-mail: ma.trujillo53@uniandes.edu.co

RECIBIDO: julio 2009 APROBADO: enero 2010

ABSTRACT:

We extend the Palia, Ravid and Wang (2008) model of family succession, and argue that family CEOs can be successful if certain characteristics, such as private knowledge, non monetary benefits from managing the firm, and personal skills are met. We use Carvajal, a large Colombian business group, to support our ideas and show that, contrary to international empirical evidence, there are certain circumstances where efforts made by heirs can be similar to those of the founder and exceed those of outside managers.

KEY WORDS:

Family businesses, successions, heirs as managers.

RESUMEN:

En este artículo extendemos el modelo de sucesión familiar de Palia, Ravid y Wang (2008), y argumentamos que los gerentes familiares pueden ser exitosos si ciertos factores se presentan, como un conocimiento tácito, beneficios no monetarios al dirigir la empresa, y el desarrollo de ciertas habilidades gerenciales personales. Utilizamos el caso de Carvajal, un importante grupo económico colombiano, para soportar nuestras ideas y mostrar que, contrario a la evidencia empírica internacional, existen ciertas circunstancias bajo las cuales los esfuerzos que hacen los herederos en la gerencia pueden ser similares a los del fundador y mayores a los de los gerentes externos.

PALABRAS CLAVE:

Empresas familiares, sucesiones, herederos como gerentes.

RÉSUMÉ:

Cet article considère le modèle de succession familiale de Palia, Ravid y Wang (2008), et l'argument consiste en ce que les gérants familiaux peuvent arriver au succès si certains facteurs se présentent, tels que la connaissance tacite, les bénéfices non monétaires dans la direction de l'entreprise, et le développement de certaines habiletés de gestions personnelles. Le cas de Carvajal est utilisé, un important groupe économique colombien, pour développer nos idées et montrer que, contrairement à l'évidence empirique internationale, il existe certaines circonstances dans lesquelles les efforts réalisés par les héritiers dans la gestion peuvent être semblables à ceux du fondateur et supérieurs à ceux de gérants externes.

MOTS-CLEFS:

Entreprises familiales, successions, gérants héritiers.

RESUMO:

Neste artigo estendemos o modelo de sucessão familiar de Palia, Ravid y Wang (2008), e argumentamos que os dirigentes familiares podem ser bem sucedidos se certos fatores apresentam-se, como um conhecimento tácito, benefícios não monetários ao dirigir a empresa, e o desenvolvimento de certas habilidades gerenciais pessoais. Utilizamos o caso de Carvajal, um importante grupo econômico colombiano, para suportar nossas idéias e mostrar que, ao contrário da evidência empírica internacional, existem certas circunstâncias sob as quais os esforços que fazem os herdeiros na direção podem ser similares aos do fundador e maiores aos dos dirigentes externos.

PALAVRAS CHAVE:

Empresas familiares, sucessões, herdeiros como dirigentes.

INTRODUCTION

Carvajal, a business group property of the Carvajal family in Colombia -with more than 100 years of history in the publishing business-, has survived various succession processes. Given the strong empirical evidence of failures of family firms managed by heirs, we raised the question: How is Carvajal different? We develop a theoretical model that shows that, under certain conditions, heirs working as managers in family businesses can exhibit behavior similar to the founder's and superior to that of outside managers. This is interesting not only in the Carvajal case, but also in the case of any family firm approaching succession.

La Porta, López de Silanes and Shleifer (1999), Claessens, Djankov and Lang (2000), Faccio and Lang (2002), among others, show that the majority of firms in the world are family-controlled. Family business literature has focused on problems related to ownership, management and control, financial performance, and succession. Research in the latter shows that founder transition plays a critical role in determining the company's future (see for example Burkart, Panunzi and Shleifer, 2003). The "succession problem" has generated an interesting debate in relation to who should occupy the top management position in a family firm (see for example Bennedsen et al., 2007).

On the one hand, arguments in favor of founder or heir management assert that enhance a firm's long term focus (Bertrand and Schoar, 2006); allow the use of specific knowledge about the company that is difficult for outsiders to obtain (Bertrand and Schoar, 2006); and, generate high levels of confidence for key stakeholders. There is also a negative relationship among family firms managed by the founder or heirs and the firms' cost of debt (Anderson and Reeb, 2003; Anderson, Sattar and Reeb, 2003). Moreover, having a manager who is the founder or a member of the founder's family can benefit families in non-monetary ways (amenity potential) (Demsetz and Lehn, 1985). Finally, family management better protects family's interests (Burkart, Panunzi and Shleifer, 2003).

On the other hand, arguments against management by the founder or members of the founder's family maintain that the manager is selected from a restricted group of individuals and it is possible that he or she does not possess the management abilities to direct the company-due to not having been educated to an appropriate level for the position and not having the necessary management skills and experience (Pérez-González, 2006). In addition, conflicts of interest among family members can undermine the organization's longevity and impede succession processes (Colli and Rose, 2003). Finally, benefits perceived for superior financial performance are blurred when the company is owned and managed by one family with multiple members, due to the complex nature of good corporate governance issues facing the business (Miller et al., 2007).

To weigh up the advantages and disadvantages of a manager who is the founder or member of the founder's family versus an outside manager, empirical studies have shown a negative relationship between firms' productivity or performance and family ownership, due to the appointment of family members as company managers (Barth, Gulbrandsen and Schonea, 2005; Sciascia and Mazzola, 2008). Contradicting these results, Maury (2006) shows that active control by family owners is associated with high profitability, and Lee (2006) finds that family firms tend to experience higher employment and revenue growth over time and are more profitable. Similar results are provided by Allouche et al. (2008) and Martínez et al. (2007). Likewise, Anderson and Reeb (2003) show that financial performance is superior in family businesses as opposed to non-family companies. Their analysis suggests that companies with the presence of the family founder show better financial and accounting performance than non-family firms. In addition, their research also shows the performance differential based on the origin of management in family businesses. Specifically, managers who are members of the family (founders or their heirs) show a positive relationship with financial profits. However, market performance appears to be better only in cases where there is the presence of a founding or outside manager. Heirs do not have this effect on the firm's market performance. Villalonga and Amit (2006) state that family ownership creates value only when the founder is the CEO or there is an outsider as CEO with the founder as chairman of the board. However, in the case of heir -CEOs a firm's value depreciates. Miller et al. (2007) comes to similar conclusions.

Morck, Shleifer and Vishny (1988) argue that in young firms the founders play an important enterprising role, while in older firms their descendants frustrate maximization of value and are too entrenched[1] to be removed. Morck, Strangeland and Yeung (2000) show that when heir's wealth is representative with respect to the country's GDP, they are entrenched and the performance of companies tends to be poor. Bennedsen et al. (2007) found that family successions have negative effects on company performance and the poor performance is particularly representative in rapidly growing industries, with a highly-trained work force and with relatively large firms. Likewise, Cucculelli and Micucci (2008) compare family-managed firms with outsider-managed firms and found a negative impact on a firm's performance and value when heirs are in control of firms in highly competitive industries. Moreover, according to Blanco-Mazagatos et al. (2007), during the first generation, lower agency costs balance the negative effect of scarce financial sources. After descendants join the firm, the increasing agency costs are compensated by more financing possibilities.

In summary, existing literature shows inferior firm performance and value when heirs are in top management positions. However, there is little in family firm literature that formally explores situations under which, given certain personal characteristics and conditions in the environment, heirs can achieve performance equal to that of the founding manager, and superior to that of outside management.

In this article, we develop a theoretical model building on the work of Palia, Ravid and Wang (2008), assuming that the founder's performance as manager is a function of his private knowledge about the firm's operations; learned management abilities; intangible, non-monetary benefit gained from directing and perpetuating his positions of power in control of the company; and his effort. In our model, heirs who are managers can achieve superior performance to outside managers. Besides, we use it to analyze the specific case of one of the bigger firms in Colombia-Carvajal. This company has had seven managers, all of them family members [2], and contrary to the literature's predictions, succession processes have been successful and have allowed the company to consolidate its position in Colombia and rapidly extend to international markets. The model and the detailed analysis of Carvajal highlight factors that influence the success of within-the-family succession processes, such as training of heirs through occupying jobs inside the company and the presence of high intangible, non-monetary benefits which may be gained from directing the firm.

This article contributes to literature of succession processes in family firms, pointing out that heirs can obtain better results than outside managers, as long as they have learned management abilities and obtain private knowledge inside the family business. The intangible, non-monetary benefit of directing the company on behalf of the family generates a high level of private benefits which are not necessarily detrimental to non-family shareholders.

The article is structured as follows. The second section (The model) presents a theoretical model adapted from Palia, Ravid and Wang (2008). The third section (Analysis of the Carvajal case) analyzes predictions of the model in the context of the Carvajal case. The fourth section concludes.

THE MODEL

Shleifer and Vishny (1989) argue that managers, seeking to perpetuate their positions, invest in specific assets that are not value-enhancing for the company as a whole, but that allow them to tie their jobs to the specificity of the assets in which they invest. On the other hand, Palia, Ravid and Wang (2008) develop a model in which the founder works with greater dedication than an outside manager, and as a result he is endogenously entrenched.[3] Their model attempts to reconcile the idea that the founders are committed workers, and that is why they become entrenched and are difficult to discharge. Therefore, within their assumptions they do not consider that the founder achieves entrenchment by specific investments that are not optimal for the company but that allow him to maintain his position of power. On the contrary, it supposes that entrenchment occurs because the founder tends to dedicate himself completely to the company's success (Palia, Ravid and Wang, 2008, p. 57). These authors refer to this entrenchment as "benevolent entrenchment".

The founder in the theoretical model

Like Palia, Ravid and Wang (2008), we formally assume that the founder, F, makes an investment, IF, in the firm's creation. The firm's value under the founder depends on the profit per unit of management production, B(IF), the function of management production of the founder, αF(·), the cost per invested unit, (p), and the units invested by him, (IF). It is important to clarify that αF(·), as a function of production, determines the level of productivity that the firm achieves under the founder's direction. The firm's value with a founding manager is expressed in equation (1) below:

Profit per unit of management production, B(I), is a function of the units invested (I). We suppose that B'(I) ≥ 0, because of which a higher unit of investment generates a higher profit per unit of management production. Besides, B''(I) < 0. This implies that there is a decrease in marginal profit with respect to the level of investment.

Building on the work of Palia, Ravid and Wang (2008) and making an extension, here we assume that α(·) is a function of private knowledge regarding the firm's operations (k), learned management abilities (s), an intangible, non-monetary benefit (r) from directing and perpetuating his positions of power in control of the company, and the effort made by management (e). According to Burkart, Panunzi and Shleifer (2003), the intangible benefit refers to private, non-monetary benefits of control, representing a return for the founder that is not obtained at the expense of company profits.[4]

Given that α(·) represents a function of management production it holds that

which implies that greater private knowledge, greater management abilities, greater intangible or non-monetary benefit, or greater effort generate greater production. In addition,

which implies that regarding these variables there is decreasing marginal productivity.

The outside manager, A, denotes the following better management alternative that the market could offer. This manager can decide about the additional investment, IA, at a cost of pIA. The firm's value with an outside manager is

in which IA≥0 and αA(·) represent the function of management production by the outside manager. It assumes that αA(·) is the function of the learned management abilities (SA). However, in general αA(·) does not depend on the variable of private knowledge, which can only be acquired by the founder or his heirs,[5] that is, kA = 0. Each company has a particular way of operating and in innovative companies or sectors with accelerated technological change, the knowledge obtained from working in the company takes on greater importance. On the other hand, αA(·) also depends on the intangible, non-monetary benefit, which in this case is always assumed to be less than when the founder manages the firm. That is, rF > rA, due to the existence of non-transferable benefits that the family founder obtains when the responsibility is assumed by a family member, such as those mentioned previously in Burkart, Panunzi and Shleifer (2003). The advantage of the founder operating investment is captured in α(·), the ability to manage the firm. It is assumed that αF(·) >αA(·), because kF(·) ≥ kA(·) and rF > rA.

Management compensation, as in Shleifer and Vishny (1989) and Palia, Ravid and Wang (2008) is a function of value added by management, that is, profit under the founder compared with profit under a new outside manager. If the founder does not add value he is replaced by an outside manager. Thus, wF, the founding manager's salary, is defined as:

The Palia, Ravid and Wang (2008)'s model assumes that investment has been made in period 1, at the time when the company started and management action is only considered in period 2, the period in which the company is in operation. pIF is taken as a hidden cost. In addition, it is assumed that the expression in brackets is fixed when the choice of effort is made. The choice of effort in period 2 determines the result of the firm's production, because of which α(·) is a function of production with effort as an input. Given that B(·) has already been determined in period 2, it can be seen as a constant that multiplies the management production level. In addition, according to the approach of Holmström (1999), it is assumed that effort generates reduced profitability for the manager. Therefore, in period 2, the founder maximizes the following equation:

The first two terms are his salary and gains made from holding shares (in which θ represents shareholder participation in the company), the third term represents the function of well-being h(·) that he experiences due to the intangible, non-monetary benefit, which is not contemplated in the original model, and the fourth term represents the cost of effort. The advantage of the founder operating the investment is expressed as:

Therefore, the founder can reach a higher level of production for each increase of effort at any point. That is, because his productivity is greater, an increase in the level of effort generates greater impact on production. The problem of maximization of (4) with respect to e is resolved by adding reasonable assumptions for the function g(·) (Holmström, 1999). These assumptions are: g'(e) ≥ 0, because of which greater management effort results in a increasing reduction of profit for the founding or outside manager, and g''(e) > 0, which determines that higher levels of effort become more costly at a growing rate. In addition, α'(e) ≥ 0 and α"(e) < 0. These characterizations provide an optimum for maximization of the founder's profit.

Consistent with Palia, Ravid and Wang (2008) we adopt the following notation

in which π(αF(e)) represents relative profitability under the founder which, given that the investment is a hidden cost, and for a specific outside manager, is only a function of effort, that is, the other variables remain constant. This transforms equation (3) into:

Maximizing equation (4) yields:

A detailed proof of equation (7) is found in the appendix. The manager balances the marginal contribution of effort with its marginal cost. For Palia, Ravid and Wang (2008), the term (f'(π(·))(1-θ)+θ) is essentially the manager's sensitivity to payment for performance, that is, the change in salaries in relation to the change in the firm's value, plus the change in wealth to the extent that it changes the firm's value. If the manager's sensitivity to pay for performance (f'(π(·))(1-θ)+θ) is noted as Y, it is possible to rewrite equation (7) as follows:

Proposition 1

For given levels of effort, (that is, the same g(e)) and for a given sensitivity to pay for performance, the founders (as characterized by equation (3)), will exercise a higher level of effort than outside managers.

Proof: See appendix.

The intuition is as follows: suppose that an outside manager optimizes to a level e*A. For this level, given the conditions in proposition 1 for the founder, the left part of equation (8) is greater than the right part of the same equation, since marginal income is still greater than the marginal cost of effort for the founder. Given the assumptions for α(·) and g(e), the founder will increase his effort until reaching its optimum, therefore the founder works more efficiently and thus generates more effort for a given set of incentives.

Proposition 1 suggests that the founders are less averse to effort. However, it is better to center the attention on what the founders are doing. They have greater clarity about innovation and the company because of having conceived it. They possess private knowledge about the firm's activities and, consistent with their personal characteristics, can pursue the maximization of the company's value with greater dedication. This proposition generates the "benevolent entrenchment" concept of Palia, Ravid and Wang (2008) we mentioned before. This is, that the founder works with greater dedication and therefore, does not respond to or need additional incentives.

Proposition 1 is essentially the same as Lemma 1 in Palia, Ravid and Wang (2008). However, we are assuming that the founder's management production function, is also a function of his private knowledge about the firm's operations; learned management abilities; intangible, nonmonetary benefit gained from directing and perpetuating his positions of power in control of the company; and his effort. This specification allows us to maintain that the founder's management production function is always above the management production function of the best outside manager, that is: αF(·) > αA(·).

The heir in the theoretical model

The advantage of the heir operating investment is equally captured in (·), the ability to manage the firm. It is assumed that αF(·) ≥ αH(·) > αA(·), where H denotes the management alternative that the family can offer through the founder's heris. As in the case of the founder, it is assumed that αH(·) is a function of the heir's private knowledge about the way the firm operates, (kH) acquired by working inside the family business; learned management abilities (SH), intangible, non-monetary benefits (rH) from directing and perpetuating positions of power for the family by controlling the business and the effort made by the heir as manager of the firm (eH).

The heir as manager, H, can make an additional investment IH, at a cost of pIH. The firm's value with an heir as manager, is expressed in equation (9)

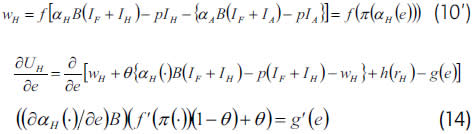

in which IH ≥ 0 and αH(·) represent the function of the managing heir's management production. His compensation is equally a function of value added by the manager, that is, profit under the heir compared to profit under an outside manager. Thus, wH, the managing heir's salary, is defined as:

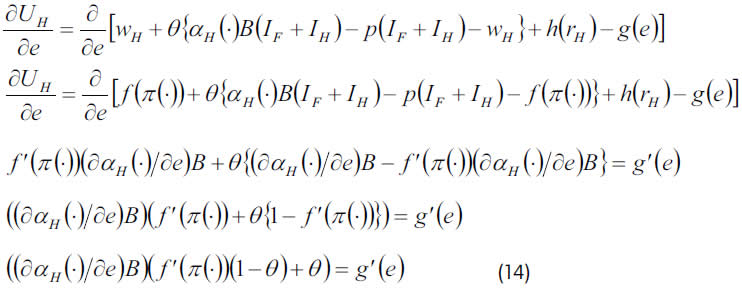

Again, pIF is taken as a hidden cost. In period 2, the heir maximizes the following equation:

The first two terms are salary and earnings due to share ownership (in which θ represents shareholder participation in the company). The third term represents the function of well-being h(·) experienced from the intangible, non-monetary benefit and the fourth term represents the cost of effort. ther heir's advantage relative to the outside manager is expressed as:

Therefore, an heir can reach a production level equal to that of the founder and always greater tha the manager's for every effort level. Note that what allows greater productivity of heirs is their private knowledge about the firm operations (k) and the intangible, non-monetary benefits (r) he can extract by managing the firm. In this model it is assumed that the heirs have learned management abilities (s) that are at least as good as those of the potential outside manager. In other words outside managers may have more formal training, but heirs has more management abilities developed through more intense in-job learning within the company. It is necessary, then, to consider the problem of maximization of (11) with respect to e. Again, for simplifying the model we adopt the following notation:

in which π(αH(e)) represents relative profit under the heir, which, given that the investment is a hidden cost and for a specific outside manager, is only a function of effort. This transforms equation (10) into

A detailed proof of equation (14) is found in the appendix. As in the case of the founder, the term (f'(π(·))(1-θ)+θ) is taken as the manager's sensitivity to pay for performance, and if this is noted as Y, equation (14) can be rewritten as follows: ((∂αH(·)/∂e)B)Y = g'(e).

Therefore, it holds that:

Proposition 2

For given levels of effort, (that is, the same g(e)) and for a given sensitivity to pay for performance, heirs (as characterized by equation (10)) will exert a higher level of effort than outside managers.

Proof: See appendix.

Following the same intuition as before, given that the marginal cost for the heir is lower than the manager's, his level of effort will be greater, at its optimum, than that exerted by the outside manager, achieving in consequence greater productivity for the firm.

Thus, the model concludes that the founder and heirs work with greater dedication and exert greater effort and therefore endogenously generate benevolent entrenchment. Note that what allows the effort to be greater in the case of the heirs is private knowledge regarding the firm's operation (k) and a greater intangible, non-monetary benefit (r), compared to the outside manager. In this way, the model predicts that a founder always achieves performance superior to that of an outside manager who is the market's best alternative. In addition, heirs as managers in family businesses can perform as effectively as the founder and better than an outside manager, as long as they have acquired specific knowledge by occupying positions within the company before being named managers, and receive high intangible, non-monetary benefits from being the manager of the family business.

The following section addresses the Carvajal case not to empirically validate the model, which of course is impossible with just one observation, but to highlight some of the model's main theoretical argumens.

ANALYSIS OF THE CARVAJAL CASE

Academic literature and media in the family business has focused on the problems affecting management succession. For example, in 2003, Dinero magazine summarized the crisis facing Danaranjo[6] after the death of David Naranjo, who founded the company in 1943 and died in 1993. This company did not succeed in carrying out a planned succession. The heirs making decisions had not previously worked in management positions within the company and conflicts of interest among family members led to the company seeking bankruptcy protection in 1999. As Dinero reported, the Danaranjo case confirms the theoretical predictions regarding the problems that arise around succession processes in family businesses (Dinero, 2003, p. 43). It is necessary, however, to take into account which factors make the difference in the story of family firms, like Carvajal, that manage to implement successful succession processes.

It is important to clarify why we consider Carvajal to be "successful". Carvajal in 1904 was just a small printing shop and now it is recognize as one of the strongest business groups in Colombia with more than 30 firms in its portfolio; it pioneer the international focus in the printing business, operate business in more than 18 countries around the world (Dinero, 2008), and all of these after seven within-family successions. Therefore the word "success" goes beyond the traditional accounting and financial measures.

We now continue with a brief historical account of the Carvajal group in order to highlight some of the key factors we think have contributed to the Carvajal "success". These factors although we recognize there could many others (e.g. political connections and rent seeking behavior), emerge directly from our theoretical.

A brief history of Carvajal[7]

Manuel Carvajal Valencia was born in 1851 in Popayán. He went to high school and university and later participaed actively in the revolutionary forces of the Conservative party in 1877 in Cali. He married Micaela Borrero in 1881 with whom he had six children: Alberto in 1882, Hernando in 1884, Manuel Antonio in 1886, Ana María in 1888, Mario in 1896 and Josefina in 1898. In 1894, Manuel Carvajal Valencia joined up with some friends to acquire an old printing press that they installed in Palmira in 1869. His motivations were more political than commercial; he founded the weekly newspaper La Opinion for defending the ideas and candidates of his political party. Manuel Carvajal interrupted his business activities during the War of a Thousand Days (1899-1901), leaving his eldest sons, Alberto and Hernando Carvajal Borrero in charge of the family. Because of these responsibilities, the two eldest boys had to leave school. On October 29, 1904, the Carvajal family business was launched in the form of a firm called Imprenta Comercial (Commercial Printing). La Opinion had ceased publication, but the family, true to its vocation, began to publish the El Dia newspaper. In 1907, Imprenta Comercial was performing well financially so Manuel Carvajal decided to create Carvajal and Co.

In 1910 Manuel Carvajal had begun to delegate the management of the company to Hernando Carvajal Borrero, the second of his sons, who had shown business skills while working in the company. In 1911 Carvajal and Cia. imported the first paper shredding machine in western Colombia and diversified into commerce. After the death of Manuel Carvajal Valencia, the presidency was held by the second of his sons, Hernando Carvajal Borrero, with the help of his older brother Alberto, from 1912 to 1939. During this period, because of the First World War, Carvajal had to deal with limited imports and had to produce and sell articles that the company had imported. The company expanded its operations to Buga and Palmira where it sold the excess products it could not sell in Cali. In 1921, Hernando Carvajal decided to travel to Europe and after several months of searching purchased the company's first lithographic printing press, which was installed by German technicians.

During the 1930s Carvajal continued to import machinery, but in 1939 with the outbreak of World War II and the impossibility of importing machinery and parts, the company set up its first mechanical department for the construction of replacement parts. The same year, Hernando Carvajal Borrero suffered a cerebral hemorrhage, so his eldest son Manuel Carvajal Sinisterra took over the company's presidency under the supervision of his uncle Mario Carvajal Borrero. At this time the company had four distinct businesses: printing, lithography, manufacture of stationery and a retail warehouse. In addition, operations began to extend to the whole country. Manuel Carvajal Sinisterra is the most important and memorialized of the presidents of Carvajal and one of the most significant figures of the Valle del Cauca region of Colombia. His first years of formal study were in Cali, but at the insistence of his uncle Alberto Carvajal he went to Belgium to continue his secondary school studies. However, because of the financial crash of 1929 he had to return to Colombia, suspend his studies and begin work for Carvajal as an employee. It is important to point out that Manuel Carvajal did not have university education. He became manager of the company at the age of 23.

The presidency of Manuel Carvajal Sinisterra, from 1939 to 1971, was characterized by the company's growth and diversification. The company benefited from State protectionism, becoming a truly national company with presence in the most important departments in Colombia and making the first inroads into other countries. One of the many outstanding projects of this period was the printing of the telephone directory for the city of Bogotá in 1958, which saw the inception of Publicar Ltda., a company based on international projection and innovation which consolidated its expansion, generating the need to acquire more sophisticated machinery later used in the Carvajal group publishing business. Before his death, Manuel Carvajal Sinisterra decided in 1969, already at an advanced age, to study business at the Massachusetts Institute of Technology (MIT). However, he died in Boston in 1971 from a heart attack.

After the death of Manuel Carvajal Sinisterra, Carvajal's CEO, the top management position was held by his brother Jaime, who managed the company from 1971 to 1979. Jaime was the first heir-president of Carvajal to have a university education. He was a civil engineer educated at the Medellin Mining School. Under his presidency Carvajal Internacional Inc. began operations in New York, transforming the company into a multinational enterprise. In addition, in 1976 the company ceased to be a limited company and became the closed corporation Carvajal. This was due to a higher number of partners as the number of founder family members had grown. Since that time, the president has not only overseen the management of the company, but he also has involved other individuals and groups such as the general shareholders' meeting, the board of directors and the chairman of the board. In 1979 Manuel Carvajal Sinisterra handed over the CEO position to Adolfo Carvajal Quelquejeu and assumed the post of chairman of the board of directors. Adolfo Carvajal Quelquejeu had a graphic arts degree from the Rochester Institute of Technology in New York (1954) and subsequently enrolled in graduate studies in administration and finance at the Universidad de los Andes. He was with the company from 1954.

The presidency of Adolfo Carvajal Quelquejeu, between 1979 and 1999, was a period of consolidation for Carvajal. He led to the first holding company in the country's history, known as Carvajal Inversiones (Carvajal Investments) in 1995, transforming the group of companies owned by the Carvajals into an economic group. In 1995, a protocol[8] to manage family relations was created, an issue which will be covered below. Adolfo Carvajal handed the CEO position to Alberto José Carvajal and was later appointed Colombian ambassador to France. Alberto Carvajal was president from 1999 to 2001. He has a degree in graphic arts engineering from Carnegie Mellon University, which he obtained in 1947. In addition, he is a 1967 graduate of the masters in industrial administration program at Universidad del Valle. Since 2001, Alfredo Carvajal Sinisterra, a 1968 graduate of the masters in industrial engineering program at the Universidad del Valle has been president of Carvajal. He did his undergraduate studies in Economics at the Wharton School of Business. Table 1 shows the succession processes at Carvajal.

The importance of private knowledge in management by heirs

Pérez-González (2006) shows that, on average, family businesses that appoint to top management positions heirs who have not received formal education in "selective" higher education institutions are characterized by poor financial performance[9]. However, these predictions are not corroborated in the Carvajal case, a company that from 1912 to 1971 was under the management of heirs, none of whom had the possibility of studying at university. During this period, Carvajal managed to extend its activities to cover the whole country, while also making incursions into international markets. On the other hand, Pérez-González states that on average heirs in management positions are younger than outside managers which he considers as evidence that family firms choose their managers based on family ties and not on merit. A young managing heir is not necessarily detrimental to a family business. It is enough to recall that Manuel Carvajal Sinisterra took over the presidency of Carvajal at age 23 after having worked several years in the company and under his management the company experienced growth, diversification and development. What could make the difference in terms of training for a managing heir to achieve excellent job performance? According to the model we developed above, private knowledge acquired by the heir inside the family business is crucial in developing his abilities as manager.

With regards to concept of knowledge we should point out that, "tacit knowledge", or "private knowledge" as referred to in the model, is when "we can know more than we can say" (Polanyi, 1966, p. 4). This "knowledge" involves personal involvement, experience, practice and imitation and is related to the idea of "learning by doing". This implies that tacit knowledge often emerges from specific ways of doing in specific contexts.

Tacit knowledge is crucial to the company's innovation capacity, its competitive advantages, and ultimately, its financial performance. The resource-based view of the firm (Penrose, 1959; Wernerfelt, 1984) holds that the organization, understood as a unique set of resources, can be the source of sustainable competitive advantages and can generate economic value, as long as it has resources that are valuable, rare, hard to imitate and without strategic equal (Barney, 1991). This leads to the perspective of a company built on knowledge; that is, the idea that knowledge is the crucial component in sustaining competitive advantage through innovation and other value-generating activities (Grant, 1996).

This knowledge, which supports the company's capacity for innovation and its competitive advantages, is what an heir acquires by working inside the company prior to assuming a top management position. This is the main advantage heirs have over an outsider when we compare their productivity in a family business. In the model presented above, the productivity of the heir (H) may equal that of the founder (F), but is always superior to that of the outside manager (A), αF(·) ≥ αH(·) > αA(·); this productivity depends on private knowledge (kH) related to the comany's operations and other variables αH(kH, sH, rH, eH).

Bertrand and Schoar (2006) are perhaps among the few authors who have recognized private knowledge as a determinant favoring selection of heirs as company managers. For them, this could occur when knowledge transmission is easier between the founder and his heirs than between the founder and an outsider. Mazzola et al. (2008) address the issue of training next-generation family members once they have joined the management team in their family firm. Their findings indicate that this involvement provides the next generation with crucial tacit business knowledge and skills, facilitating interpersonal work relationships between incumbents and next-generation leaders and building credibility and legitimacy for the next generation. Moreover, observations in the case of Carvajal contradict the arguments of Morck, Stangeland and Yeung (2000), Pérez-González (2006), and Burkart, Panaunzi and Shleifer (2003), which maintain that family management is generally less efficient than "professional management". Likewise, they contradict the results of Volpin (2002), who found that when controlling shareholders are involved in the company's management, corporate governance and financial performance tend to be poor. Finally, the success of heirs in Varvajal and their longevity in the company's management coincides with the findings of Smith and Amoako-Adu (1999), who show good financial performance when succession processes favor heirs rather than outside managers.

In the Carvajal case, all heirs that became CEOs have been involved with company operations for several years before assuming top management positions. The two first managing heirs, Hernando Carvajal Borrero (CEO 1912-1939) and Manuel Carvajal Sinisterra (CEO 1939-1971) were trained in the company from a very young age, despite lacking university education. The innovative tradition of Carvajal could have become critical "private knowledge". As summarized, in 1911 the company imported the first paper shredding machine, in 1921 the first lithographic printing press, and it has continued to import the latest technology to the present day. In addition, in 1939 the company developed its first mechanical department for construction of spare parts. Due to the specificity of the assets used, the knowledge acquired by heirs in their early involvement Carvajal's business operations, is of great importance for their later success in management.

The Danaranjo case, also mentioned above, is a good counterexample to what occurred in the case of Carvajal. David Naranjo had six sons, of which the three eldest predeceased the founder. The three remaining sons had practically no participation in the company's activities until 1993, the year that David Naranjo died. Their lack of specific business experience was one of the factors that led the company to seek bankruptcy protection in 1999.

Intangible, non-monetary benefit

The term "amenity potential" was first proposed by Demsetz and Lehn (1985). These authors argue for the existence of a non-pecuniary gain brought about by the company name. Obtaining the amenity potential contributes to maximizing ownership benefits, even if it does not deliver profit maximization to all shareholders. As we mentioned earlier, Burkart, Panunzi and Shleifer (2003) state that a founder could obtain non-monetary benefits from having a son directing the company that bears the family name. Alternatively, in some industries, such as sports or communications, families can participate in or influence social, political, and cultural events through ownership of the firms. Ehrhardt and Nowak (2001) conclude that if the intangible, non-monetary benefit is representative, families will attempt to retain control of their firms as far as possible.

The intangible, non-monetary benefit is easily identifiable when analyzing the Carvajal case. The company came into being because of the political interests of Manuel Carvajal Valencia, probably ahead of his business interests. As mentioned, in 1894 Manuel Carvajal clubbed together with some friends to purchase an old printing press and publish the La Opinion weekly newspaper, to promote the ideas and candidates of their political party. Subsequently, in 1904 the Carvajals began to publish the El Dia newspaper. Through these media the family waged campaigns for the creation of the Department of Valle del Cauca and the Diocese of Cali, objectives that they achieved in 1910. Manuel Carvajal took up a seat in the newly created Departmental Assembly, and later became the department's Director of Public Instruction, while Hernando Carvajal Borrero's (1896-1972) brother was ambassador to Ecuador, rector of the Universidad del Valle for three years and Minister of Education. Manuel Antonio Carvajal was ambassador to Perú, Bolivia, Uruguay, and Paraguay, as well as Governor of Valle del Cauca.

Manuel Carvajal Sinisterra, third president of Carvajal, was Minister of Mines and Petroleum, a period that saw the creation of Empresa de Petróleos de Colombia -Ecopetrol (1951). Subsequently, he was Minister of Communications. He founded or participated in the creation of entities such as the Federation for Higher Education and Development - Fedesarrollo-, the Foundation for Higher Education -FES- and the Industrial Association -ANDI-, among others. He was awarded the Cruz de Boyacá, Medalla al Mérito Industrial de la Nación (National Medal of Industrial Merit) and an honorary doctorate in social sciences and economics from the Universidad del Valle.

The social recognition that family members have enjoyed represents a high intangible, non-monetary benefit that the Carvajals have enjoyed since inception. The model presented in this article assumes that this benefit constitutes another of the advantages for the company to be led by heirs rather than by outside management. The productivity of the heir (H), denoted as αH(kH, sH, rH, eH), which depends on the intangible, non-monetary benefit (rH ), makes it for the firm possible to achieve better financial performance when it is managed by a family member, as long as the intangible, non-monetary benefits are representative.

Another reason to preserve family control is reputation. The benefits of good reputation could be lost if company management is ceded to an outsider (Burkart et al., 2003), for example, the economic reputation obtained from the positioning of the company's products in terms of quuality. Faccio (2002) carried out a study in 42 countries and found that companies that have political connections are relatively numerous and that these connection impact positively on financial performance. Faccio considered a firm as politically-connected if a controlling shareholder or director is a member of parliament, minister, chief of state or closely related to a high-level politician.

It's important to acknowledge that Carvajal's political connections could have had a relevant effect in the success of the company. This family has always been involved in the most important Colombian political circles and that could bring out some benefits for them. We highlighted previously that many others factors could contribute to the Carvajal "success" (e.g. political connections and rent seeking behavior).

Up to now it is apparent how variables of private knowledge and intangible, non-monetary benefits could cause the productivity of the managing heir to be superior to that of an outside manager. However, it is pertinent to ask if the family's growth and the increase in the number of generations and heirs influence the high productivity enjoyed by heirs. This discussion is pertinent to the extent that some authors have argued the incidence of these factors in the productivity of managers related to the founder's family. We address this issue next.

Learned management abilities

The family's evolution involves a change in the heirs' level of education. In the first two successions, managers do not have university education. In the case of Carvajal, it is clear how over time the managing heir resembles the outside manager. The frustration experienced by the first managing heirs from not completing their university studies was not an issue for the four most recent generations of the dynasty. Jaime Carvajal (CEO 1971-1979) did his undergraduate studies in the country, while Adolfo Carvajal Quelquejeu (CEO 1979-1999), Alberto José Carvajal (CEO 1999-2001), and Alfredo Carvajal Sinisterra (CEO 2001-2008) earned their undergraduate degrees abroad and undertook their graduate studies in Colombia, attending highly prestigious educational institutions.

In the model developed above, it is assumed that the heirs have learned management abilities (s) at least equal to those potential outside managers. This assumption is based on the Carvajal case: In the first generations, heirs had no opportunity to acquire management abilities in a formal way. Nevertheless, their work experience inside the company and specific knowledge about the handling of highly specialized imported machinery are examples of learned management abilities that are of great practical importance and it is the result of on-the-job training. These on-the-job skills compare favorably with the formal education of the outside manager. Over time, learned management abilities acquired through working at the company lose value to the extent that the organization grows, processes standardize and their complexity does not permit appropriation of a deep, differentiating knowledge about each of the many company's activities. However, more recent heir's formal training is comparable to that obtained by the outside manager. Both are university-trained.

Increase in the number of generations and heirs

When Manuel Carvajal Valencia founded his company he had a family consisting of his wife and six sons. Under Jaime Carvajal Sinisterra's management (CEO 1971-1979), the company changed from a limited company to a corporation, due to the growing number of heirs as shareholders. On the other hand, under Adolfo Carvajal Quelquejeu's management (CEO 1979-1999) a protocol was developed to manage family relations. This protocol, created in 1995, established norms for resolving family conflicts and clearly managing the relationship between companies and their heir partners. Among other things, it also established procedures for selling shares, services that the company could provide to heirs, prohibited the Carvajals from competing with family businesses and created the family committee in charge of monitoring compliance with these norms, counseling the family and ensuring the heirs' well-being.

The Family Council has a board of directors made up of all the Carvajals over eighteen years of age. This council is the entity through which members of the family are presented if they wish to join the organization, and compete for jobs among themselves and with outsiders. In addition, it provides support to family members who have problems. The protocol was circulated in writing, expecting all the heirs would sign it. Given the growth in the number of family members, it is valid to question how this affects the managing heir, compared with an outsider in the same position.

The choice of a managing heir is justified to reduce agency problems when an outside manager is appointed and seeks to extract private benefits (Bertrand and Schoar, 2006; Burkart, Panunzi and Shleifer, 2003). Private benefits from managing the company, as described by Jensen and Meckling (1976) generate expenses from the profits of outside shareholders. Therefore, to hand over control of the company to outside management exposes the family to possible expropriation of a portion of its wealth. This suggests that heirs are in a better position to watch over family interests and focus on maximizing the company's value without the risk of appropriation of private monetary benefits. However, a very different situation confronts the managing heir belonging to the second generation, who must answer to his father and brothers for the company's results. He must also answer for the company's management to more than 200 heirs who are partners. This situation could cause the same agency problem as that confronting an outside manager.

The dilution of benefits with respect to the agency problem and the similarity of heirs to outsiders could be why Carvajal has designed selection mechanisms guaranteeing competency for job positions between themselves and outside candidates. It appears that with the increase in the number of generations and heirs, their performance in management is far from that achieved by the founding manager and similar to that obtained by outside managers.

It is possible that the growth of the companies, the formalization of duties, standardization of processes and the competence and symmetry of information among family members affect benefits in terms of private knowledge and intangible, non-monetary benefits, and increase the threat of expropriation of private monetary benefit.

The relationship between the founding manager, the managing heir and the outside manager over time and the increase in the number of generations and members of the family is shown in Figure 1. When this occurs, the heir's performance as management is far from being as effective as that of the founding manager, but close to that of outside managers. It is possible that the growth of companies, formalization of duties and standardization of processes, as well as the reliability and symmetry of information shared by members of the family, affect benefits in terms of private knowledge and intangible, non-monetary benefits, and increase the threat of expropriation of private monetary benefits.

The preceding statement could find support in Miller et al. (2007). These authors state that depending on the definition used for family business, various empirical results can be found regarding these firms's financial performance. For some authors a family business is any company controlled and directed by multiple members of a founding family (Shanker and Astrachan, 1996), while for others it is when the company is directed and owned by a founder without participation by other family members. (Anderson and Reeb, 2003; Faccio and Lang, 2002; Smith and Amoako-Adu, 1999). According to Miller et al. (2007), the average performance of family firms is better when it is owned by multiple family members; that group of firms shows returns similar to those of non-family firms with similar characteristics.

EMPIRICAL PREDICTIONS

Before stating some of the empirical prediction of our analysis, we present several international examples that stress our main point in this paper. We posit that an heir could become as good a manager as the founder if he or she could gain private knowledge about business affairs not easily learned outside the firm. Also, the non-financial benefits he or she may gain when running the family firm give them a higher utility level when compared to outside managers (see section 2).

These theoretical arguments which help us to better understand the Carvajal case, may also be recognized in other family firms around the world. Bulgari, a well-known producer of luxury goods with more than 236 stores worldwide, is a good example (Bulgari, 2009). It was founded in 1884 in Rome by Sotirio Bulgari, and his two sons, Constantino and Giorgio Bulgari developed a great interest and involvement in the family business. They were responsible for taking Bulgari to the international market (New York, Paris, Geneva and Monte Carlo). In 1984 the third within family succession took place, bringing with it a period of great growth and diversification. In 1995 Bulgari was listed on the Italian Stock Exchange.

There are many other examples of successful within-family successions. Gonzalo Comella, founded in 1870, is among the most well-known clothing stores in Barcelona, Spain (Gonzalo Comella, 2009). The firm is currently run by the fourth generation with three brothers in top management positions. The fifth generation is currently working in midlevel management, getting experience to run the firm in the future.

Three more examples will help to make our point: E&G Gallo Winery, a wine producer, Faber-Castell Company, a writing instruments maker, and Kruss Optronic, precision optical instruments manufacturer. The first of these three firms was founded in 1933 by two brothers Ernest and Julio Gallo, and four generations have passed through the company management making E&G Gallo Winery the biggest wine producer in U.S. exporting to more than 90 countries around the world (E&G Gallo Winery, 2009). Faber-Castell Company was founded in 1761 and today is run by the eighth generation. Lothar Faber (fourth generation) was responsible for the international growth of the company when he took over at the age of 22, but having previously gained experience in Paris and London in the writing instrument business (Faber-Castell Company, 2009). Finally, Kruss Optronic, also run by the eighth generation, has always been at the cutting edge of optometric innovation since its inception, with family members actively involved in the German scientific community and related business associations.

All these examples represent anecdotic evidence that support some of the main points we hoped to highlight in our model and in the Carvajal case: family reputation and specific knowledge from within the firm in specialized industries are among the key drivers for successful succession in family business. Therefore this analysis should not be interpreted as a "proof" of the model, but as a conceptual validation of our ideas.

As we said, the Carvajal case analyzed here and these examples allow us to give conceptual support for our model; however, the theory we developed could also be validated empirically in order to gain also statistical support. Specifically, the model proposes the following concrete empirical hypotheses:

- Firms in specialized industries, in which private knowledge is determinant for business success, will have better financial performance if managed by family members.

- Firms managed by heirs who did not work in the family business prior to becoming CEO, will show inferior financial performance.

- Family businesses which are politically-connected, will favor heirs for top management positions.

CONCLUSION

All the successful successions in Carvajal run contrary to literature's theoretical and empirical evidence. Descendants in the Carvajal family with leading responsibilities did not frustrate the company's economic growth and did not destroy their ancestors' wealth. On the contrary, they consolidated the firm over time, expanding it into a group with considerable relevance to the Colombian economy. This case presents arguments in favor of the idea that the benefits of a founder-CEO, under certain conditions, could be extended to an heir-CEO. These include the presence of private knowledge crucial to company success and an intangible, non-monetary benefit for the family. Ultimately, it can be expected that like a founding CEO, a managing heir can make use of specific knowledge about the firm that is difficult for outsiders to obtain, thus generating high levels of confidence with key interest groups within and outside the firm. In addition, heirs can benefit families to the extent that there is an intangible, non-monetary benefit from directing and perpetuating positions of power in the firm, which can protect the family's interest in a weak investor protection environment. It also lowers the risk of appropriation of cash flows by an outside manager.

On the other hand, it is possible that the heir, like the founding manager, will employ a long-term strategy, thus avoiding "management myopia" (Stein, 1988; 1989). According to this author, managers avoid assuming long-term projects that could have low short-term returns, for fear that the market will incorrectly interpret this financial performance and he will lose his job, or face hostile takeover threats. Family management is less worried about the market reactions of business decisions. Zellweger (2007) states that family firms display longer-term horizons than most of their nonfamily counterparts since family firms hold longer CEO tenure and this firm will strive for long-term independence and succession within the family.

Finally, growth in the number of generations and heirs of the founder's family affect the managing heir's performance, mitigating the advantages with respect to the agency problem in relation to appointing the manager. On the other hand, a greater number of heirs imply competency due to access to jobs, a greater level of meritocracy and preparation of heirs which is similar to that of outsiders in terms of formal education. Therefore, under these situations the heir's performance is a long way from being as effective as the founder's performance, but close to that of an outside manager.

Appendix

From equation (7):

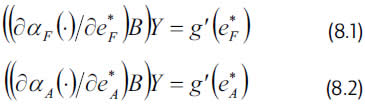

Proof of Proposition 1

From equation (8) it holds that ((∂αF(·)/∂e)B)Y = g'(e), and additionally, from equation (5) it is known that for all optimal effort

.

.Departing from this, it is possible to establish two equations where the founder and the outside manager equalize their marginal cost and their marginal income from effort:

.

.Subtracting equation 8.2 from equation 8.1, it holds that

.

.Because of (5) that the left part of equation (8.3) is greater than zero. Therefore,

.

.and knowing that and, then

.

.

Deduction of equation (14)

.

.

Proof of Proposition 2

From equation (15), it holds that ((∂αH(·)/∂e)B)Y = g'(e), and in addition, from equation (12) it is known that for all optimal effort

Starting from this, it is possible establish two equations where the heir and the outside manager equalize their marginal cost and their marginal income from effort:

Subtracting equation 15.2 from 15.1 it holds that

From (12), it is known that the left part of equation (15.3) is greater than zero. Finally

and knowing that g'(e) > 0 and g"(e) > 0, then

FOOTNOTES

[1] Some authors, such as Shleifer and Vishny (1989), show that managers seek to perpetuate their positions and therefore take actions that make it difficult to remove them from their positions, such as investing in specific assets that favor their permanence in the company. When this occurs, it is called "entrenchment" of the individuals in positions of power.

[2] In 2008, and after 104 years of history in the business, Carvajal appointed, for the first time, an outsider as CEO- Ricardo Obregón. The impact of this decision is hard to analyze just yet given the proximity of the event. However, it will be an interesting issue to address in the future.

[3] Because the founder exerts a high level of effort, there is a greater possibility of displaying better performance than with any other manager. This, accompanied by the specific knowledge that the founder possesses regarding the company's purpose, generates an indirect entrenchment, that is, an endogenous entrenchment.

[4]"A founder can obtain the pleasure of having his son directing the company that carries the family name. Alternatively, in some industries, such as sports or communication media, families can participate in or influence social, political and cultural events through ownership of the companies. This reason for family control suggests that there is a distribution of patterns of ownership inside the country, with companies generating considerable intangible, non-monetary benefits for the families that control them." (Burkart, Panunzi and Shleifer, 2003, p. 2168).

[5] When we refer to an outside manager, we make reference to an executive who does not belong to the family. If this kind of executive has not worked in the company previously, αA(·) does not depend on the variable of private knowledge. For example, experience acquired from working in the company from the beginning of one's working life, specific knowledge derived from using the technologies developed by the organization, understanding of the culture and organizational climate, among others. However, on some occasions, an outside manager may have worked previously in the company, and may manage to acquire part or all of the private knowledge that an heir may be able to acquire.

[6] Danaranjo is a recognized company in the printing and graphic arts sector in Colombia. The company set up in 1943 in Bogotá. In 1960 it opened branches in Medellin and Barranquilla. In 1964 it imported machinery for making notebooks. In the same year it began making office stationery supplies. In 1970 it created its continuous forms division, a product that is to this day only offered by Carvajal. In the same decade Danaranjo entered another business that it now dominates: printing of securities instruments. In the eighties, the company participated in the telephone directory market with the printing of the Pereira directory, a product introduced in 1958 in Colombia by Carvajal. Currently its head office is in Bogotá, with branches in Medellin, Barranquilla, Cali, Pereira, Bucaramanga, Cucuta, Neiva, Ibagué, Tunja, Rioacha, and Barrancabermeja. In addition, it is run by an outside manager. Source: Danaranjo S.A. (2008).

[7] Information in this section is taken from Vanegas (2003).

[8] A protocol is a guide for making decisions. It is a document or written agreement that brings together family, company and ownership interests taking into account legal, economic, business, psychological and emotional components of the family. The elements in a Family Protocol must be: the family, signatories, generations and possible ramifications, the company's history and its traditional and business values, principal governance organs and their configuration. A family protocol also includes basic standards for incorporation of a family business, compensation policies, dividends, participation and ownership. Also, succession policy, separation, divorce, usufruct, business and company performance, social responsibility among public objectives and potentials, correlation between commercial image and family image and potentially risky operations are also considered in the document. The protocol covers critical succession processes, family business incorporation, compensation and ownership policies, methods of resolving conflict that ensure family harmony, the company's responsibilities to family members and contingency plans, among others. Source: Family Business Institute (2008).

[9] According to Pérez-González (2006) a "selective" university in the United States is an institution classified as "very competitive," according to the profiles defined by Barron (1980). In 1980, a total of 189 universities that considered the top 50% of students in their graduation classes as qualified for admission, were classified as very competitive.

REFERENCES

Allouche, J., Amann, B., Jaussaud, J. & Kurashina, T. (2008). The impact of family control on the performance and financial characteristics of family versus nonfamily businesses in Japan: A matched-pair investigation. Family Business Review, 21(4), 315-329.

Anderson, R. & Reeb, D. (2003). Founding-Family Ownership and Firm Performance: Evidence from the S&P 500. Journal of Finance, 58, 1301-1327.

Anderson, R., Mansi, S. & Reeb, D. (2003). Founding family ownership and the agency cost of debt. Journal of Financial Economics, 65, 263-285.

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99-120.

Barron's Educational Series, Inc. (1980). Barron's profiles of American Colleges. Hauppauge: Barron's Educational Series, Inc.

Barth, E., Gulbrandsen, T. & Schønea, P. (2005). Family ownership and productivity: The role of owner-management. The Journal of Corporate Finance, 11(1-2), 107-127.

Blanco-Mazagatos, V., De Quevedo-Puente, E. & Castrillo, L. (2007). The trade-off between financial resources and agency costs in the family business: An exploratory study. Family Business Review, 20(3), 199-213.

Bertrand, M. & Schoar, A. (2006). The role of family in family firms. Journal of Economic Perspectives, 20, 647-691.

Bennedsen, M., Nielsen, K.N., Pérez-González, F. & Wolfenzon, D. (2007). Inside the family firm: The role of families in succession decisions and performance. Quarterly Journal of Economics, 20(2), 647-691.

Bulgari. (2009). Historia de Bulgari, Retrieved February 11, 2009, http://www.bulgari.com

Burkart, M., Panunzi, F., and Shleifer, A. (2003). Family firms. Journal of Finance, 58, 2167-2202.

Claessens, S., Djankov, S., & Lang, L. (2000). The separation of ownership and control in East Asian corporations. Journal of Financial Economics, 58, 81-112.

Colli, A. & Rose, M. (2003). Family firms in a comparative perspective. En Franco Amatori & Geoffrey Jones (Eds.), Business history around the world (pp. 339-352). Cambridge: Cambridge University Press.

Cucculelli, M. & Micucci, G. (2008). Family succession and firm performance: Evidence from Italian family firms. The Journal of Corporate Finance, 14(1), 17-31.

Danaranjo S.A., (2008). Historia de Danaranjo S.A. Retrieved May 19, http://www.lasamarillaseninternet.com/

Demsetz, H. & Lehn, K. (1985). The structure of corporate ownership: Causes and consequences. Journal of Political Economy, 93, 1155- 1177.

Dinero Magazine. (1994, November). ¿Cuáles son los grupos o conglomerados empresariales que siguen en importancia a los cuatro más grandes? Revista Dinero, 19, 24-32.

Dinero Magazine. (2003, August 8). La trampa familiar. Revista Dinero, 187, 42-48.

Dinero Magazine. (2008, September 12). Alfredo Carvajal Sinisterra. Revista Dinero, 310, 190.

E & J. Gallo Winery. Nuestra familia. Retrieved February 11, http://www.gallo.com/family/OurFamily.html

Ehrhardt, O. & Eric Nowak. (2001). Private benefits and minority shareholder expropriation-Empirical evidence from IPOs of German family owned firms, CFS Working Paper 2001/10.

Faber-Castell. (2009). La historia de Faber-Castell Company. Retrieved February 11, http://www.faber-castell.de/17143/The-Company/History-of-the-company/index.aspx

Faccio, M. (2002). Politically-connected firms: Can they squeeze the State? Working paper series, National Bureau of Economic Research.

Faccio, M. & Lang, L. (2002). The ultimate ownership of Western European corporations. Journal of Financial Economics, 65, 365-395.

Grant, R. (1996). Toward a knowledge-based theory of the firm. Strategic Management Journal, 17, 109-122.

Gonzalo Comella. (2009). Fundación de Gonzalo Comella. Retrieved February 11, http://www.gonzalocomella.com

Holmström, B. (1999). Managerial incentive problems: A dynamic perspective. Review of Economic Studies, 66(1), 169-182.

Instituto de la Empresa Familiar. (2008). Introducción al protocolo familiar (introduction to the family protocol). Retrieved May 19, http://prensa.iefamiliar.com/.

Jensen, M. & Meckling, W. (1976). Theory of the firm: Managerial behavior, agency costs and capital structure. Journal of Financial Economics, 3, 305-360.

Krüss Optronic. (2009). Historia. Retrieved February 11, http://www.kruess.com/

La Porta, R., López-de-Silanes, F. & Shleifer, A. (1999). Corporate ownership around the world. Journal of Finance, 54(2), 471-517.

Lee, J. (2006). Family firm performance: Further evidence. Family Business Review, 19(2), 103-114.

Martínez, J.B.S. & Quiroga, B. (2007). Family ownership and firm performance: Evidence from public companies in Chile. Family Business Review, 20(2), 83-94.

Maury, B. (2006). Family ownership and firm performance: Empirical evidence from Western European corporations. The Journal of Corporate Finance, 12(2), 321-341.

Mazzola, P., Marchisio, G. & Astrachan, J. (2008). Strategic planning in family business: A powerful developmental tool for the next generation. Family Business Review, 21(3), 239-258.

Miller, D., Le Breton-Miller, I., Lester, R. & Cannella Jr., A. (2007). Are family firms really superior performers? The Journal of Corporate Finance, 13(5), 829-858.

Morck, R., Shleifer, A. & Vishny, R. (1988). Management ownership and market valuation: An empirical analysis. Journal of Financial Economics, 20, 293-315.

Morck, R., Stangeland, R. & Yeung, B. (2000). Inherited wealth, corporate control, and economic growth. In Morck Randall (Ed.), Concentrated Corporate Ownership. NBER Conference Volume. Chicago, IL: University of Chicago Press.

Palia, D., Ravid, A. & Wang, C.J. (2008). Founders versus non-founders in large companies: Financial incentives and the call for regulation. Journal of Regulatory Economics, 33, 55-86.

Penrose, E. (1959). The theory of the growth of the firm. New York: John Wiley.

Polanyi, M. (1966). The tacit dimension. New York: Doubleday.

Pérez-González, F. (2006). Inherited control and firm performance. American Economic Review, 96(5), 1559-1588.

Sciascia, S. & Mazzola, P. (2008). Family involvement in ownership and management: Exploring nonlinear effects on performance. Family Business Review, 21(4), 331-345.

Shanker, M. & Astrachan, J. (1996). Myths and realities: Family businesses' contribution to US economy - A framework for assessing family business statistics. Family Business Review, 9(2), 107-123.

Shleifer, A. & Vishny, R. (1989). Management entrenchment: The Case of Manger-Specific Investments. Journal of Financial Economics, 25, 123-139.

Smith, B. & Amoako-Adu, B. (1999). Management succession and financial performance of family controlled firms. The Journal of Corporate Finance, 5(4), 341-368.

Stein, J. (1988). Takeover threats and managerial myopia. Journal of Political Economy, 96(1), 61-80.

Stein, J. (1989). Efficient capital markets, inefficient firms: A model of myopic corporate behavior. Quarterly Journal of Economics, 104(4), 655-669.

Vanegas, C.A. (2003). Evolución del Grupo Carvajal 1904-2002. Tesis de maestría. Universidad de los Andes, Bogotá, Colombia. Inédita.

Villalonga, B. & Amit, R. (2006). How do family ownership, control and management affect firm value? Journal of Financial Economics, 80(2), 385-417.

Volpin, P. (2002). Governance with poor investor protection: Evidence from top executive turnover in Italy. Journal of Financial Economics, 64(1), 61-90.

Wernerfelt, B. (1984). A resource-based view of the firm. Strategic Management Journal, 5, 171-180.

Zellweger, T. (2007). Time Horizon, costs of equity capital, and generic investment strategies of firms. Family Business Review, 20(1), 1-15.

Cómo citar

APA

ACM

ACS

ABNT

Chicago

Harvard

IEEE

MLA

Turabian

Vancouver

Descargar cita

Visitas a la página del resumen del artículo

Descargas

Licencia

Derechos de autor 2010 Innovar

Esta obra está bajo una licencia internacional Creative Commons Reconocimiento-NoComercial-CompartirIgual 3.0.

Todos los artículos publicados por Innovar se encuentran disponibles globalmente con acceso abierto y licenciados bajo los términos de Creative Commons Atribución-No_Comercial-Sin_Derivadas 4.0 Internacional (CC BY-NC-ND 4.0).

Una vez seleccionados los artículos para un número, y antes de iniciar la etapa de cuidado y producción editorial, los autores deben firmar una cesión de derechos patrimoniales de su obra. Innovar se ciñe a las normas colombianas en materia de derechos de autor.

El material de esta revista puede ser reproducido o citado con carácter académico, citando la fuente.

Esta obra está bajo una Licencia Creative Commons: