Publicado

NGOs EFFICIENCY AND TRANSPARENCY POLICY: THE COLOMBIAN CASE

POLÍTICA DE EFICIENCIA Y TRANSPARENCIA EN LAS ONG: EL CASO COLOMBIANO

POLÍTICA DE EFICIÊNCIA E TRANSPARÊNCIA NAS ONG: O CASO COLOMBIANO

DOI:

https://doi.org/10.15446/innovar.v26n60.55534Palabras clave:

Transparency, efficiency, NCOs, Internet (en)Transparencia, eficiencia, ONG, Internet (es)

Transparência, eficiência, ONG, internet (pt)

Descargas

In recent years the influence of Colombian non-governmental organizations (NCOs) in diverse social sectors of the country has increased. However, the legitimacy of this sector has been undermined by corruption. This distrust has questioned the efficiency of NCOs as social tools. Transparency as a mechanism against corruption and one of the tools that improves the functioning of an organization is considered. There is no doubt that Internet is an essential element in disseminating information to the different stakeholders of the organization.

This paper sets out three main objectives: i) the analysis of information disclosure through the Internet of Colombian NCOs, ii) the analysis of the efficiency of these entities in reaching their social goals and, iii) the analysis of the online transparency effect in a greater efficiency of the Colombian NCOs.

En los últimos años se ha evidenciado un incremento de la influencia de las Organizaciones No Gubernamentales (ONG) colombianas en diversos sectores de la sociedad. No obstante, la legitimidad de este tipo de organizaciones se ha visto desdibujada por la corrupción, originando cierta desconfianza en su labor y cuestionamientos sobre su eficiencia como herramienta social. Por su parte, la transparencia es considerada como un mecanismo anti-corrupción y una de las herramientas para el mejoramiento en la gestión de estas organizaciones; no cabe duda de que el Internet es un elemento clave para la diseminación de información a las diferentes partes interesadas. Por tal razón, este artículo se plantea tres objetivos: i) analizar la divulgación de información a través del Internet por parte de las ONG colombianas, ii) analizar la eficiencia de estas entidades en la consecución de sus objetivos sociales y iii) analizar el efecto de la transparencia en línea sobre una mayor eficiencia de las ONG en Colombia.

DOI: https://doi.org/10.15446/innovar.v26n60.55534

Ética Empresarial y Responsabilidad Social

NGOs EFFICIENCY AND TRANSPARENCY POLICY: THE COLOMBIAN CASE

POLÍTICA DE EFICIENCIA Y TRANSPARENCIA EN LAS ONG: EL CASO COLOMBIANO

POLÍTICA DE EFICIÊNCIA E TRANSPARÊNCIA NAS ONG: O CASO COLOMBIANO

LA POLITIQUE DE L'EFFICACITÉ ET DE LA TRANSPARENCE DANS LES ONG: LE CAS DE LA COLOMBIE

María del Mar Gálvez RodríguezI, Carmen Caba PérezII, Manuel López GodoyIII

I Doctora en Ciencias Económicas Universidad de Almería

Almería, España

Nuevos Enfoques en Finanzas y Sistemas de Información Empresarial (SEJ385)

Correo electrónico: margalvez@ual.es

Enlace ORCID: https://orcid.org/0000-0002-3708-6229

II Doctora en Ciencias Económicas Universidad de Almería

Almería, España

Nuevos Enfoques en Finanzas y Sistemas de Información Empresarial (SEJ385) Correo electrónico: ccaba@ual.es

Enlace ORCID: https://orcid.org/0000-0002-8452-5909

III Doctor en Ciencias Económicas Universidad de Almería

Almería, España

Nuevos Enfoques en Finanzas y Sistemas de Información Empresarial (SEJ385)

Correo electrónico: malopez@ual.es

Enlace ORCID: https://orcid.org/0000-0001-6233-1073

Correspondencia: Universidad de Almería. Cr. Sacramento s/n. CP 04120. La Cañada (Almería), España.

Citación: Gálvez Rodríguez, M., Caba Pérez, C., & López Godoy, M. (2016). NGOs Efficiency and Transparency Policy: The Colombian Case. Innovar, 26(60), 67-82. doi: 10.15446/innovar.v26n60.55534.

Clasificación JEL: L31, G14, D61.

Recibido: Julio 2013, Aprobado: Junio 2014.

Abstract:

In recent years the influence of Colombian non-governmental organizations (NCOs) in diverse social sectors of the country has increased. However, the legitimacy of this sector has been undermined by corruption. This distrust has questioned the efficiency of NCOs as social tools. Transparency as a mechanism against corruption and one of the tools that improves the functioning of an organization is considered. There is no doubt that Internet is an essential element in disseminating information to the different stakeholders of the organization.

This paper sets out three main objectives: i) the analysis of information disclosure through the Internet of Colombian NCOs, ii) the analysis of the efficiency of these entities in reaching their social goals and, iii) the analysis of the online transparency effect in a greater efficiency of the Colombian NCOs.

Keywords: Transparency, efficiency, NCOs, Internet.

Resumen:

En los últimos años se ha evidenciado un incremento de la influencia de las Organizaciones No Gubernamentales (ONG) colombianas en diversos sectores de la sociedad. No obstante, la legitimidad de este tipo de organizaciones se ha visto desdibujada por la corrupción, originando cierta desconfianza en su labor y cuestionamientos sobre su eficiencia como herramienta social. Por su parte, la transparencia es considerada como un mecanismo anti-corrupción y una de las herramientas para el mejoramiento en la gestión de estas organizaciones; no cabe duda de que el Internet es un elemento clave para la diseminación de información a las diferentes partes interesadas. Por tal razón, este artículo se plantea tres objetivos: i) analizar la divulgación de información a través del Internet por parte de las ONG colombianas, ii) analizar la eficiencia de estas entidades en la consecución de sus objetivos sociales y iii) analizar el efecto de la transparencia en línea sobre una mayor eficiencia de las ONG en Colombia.

Palabras-clave: Transparencia, eficiencia, ONG, Internet.

Resumo:

Nos últimos anos, evidenciou-se um aumento da influência das Organizações não Governamentais (ONG) colombianas em diversos setores da sociedade. No entanto, a legitimidade desse tipo de organizações foi desconfigurada pela corrupção, o que originou certa desconfiança em seu trabalho e questionamentos sobre sua eficiência como ferramentas sociais. Por sua parte, a transparência é considerada como um mecanismo anticorrupção e uma das ferramentas para o melhoramento na gestão dessas organizações; não há dúvidas de que a internet é um elemento-chave para a disseminação de informação para as diferentes partes interessadas. Por tal razão, este artigo apresenta três objetivos: i) analisar a divulgação de informação por meio da internet por parte das ONG colombianas, ii) analisar a eficiência dessas entidades na realização de seus objetivos sociais e iii) analisar o efeito da transparência on-line sobre uma maior eficiência das ONG na Colômbia.

Palavras-chave: Transparência, eficiência, ONG, internet.

Résumé:

Au cours des dernières années, il est évident que l'influence des organisations non gouvernementales (ONG) dans les différents secteurs de la société colombienne a augmenté. Cependant, la légitimité de ces organisations a été brouillée par la corruption, ce qui est à l'origine d'une certaine méfiance envers leur travail et la mise en question de leur efficacité en tant qu'outils sociaux. D'autre part, la transparence est considérée comme un mécanisme anti-corruption et un outil pour améliorer la gestion de ces organisations. Il n'y a aucun doute que l'Internet est un élément clé pour la diffusion de l'information entre les différentes parties prenantes. Pour cette raison, cet article se propose trois objectifs: i) analyser la diffusion des informations des ONG colombiennes à travers l'Internet ; ii) d'analyser l'efficacité de ces entités dans la réalisation de leurs objectifs sociaux ; et iii) analyser l'effet de la transparence en ligne sur une plus grande efficacité des ONG en Colombie.

Mots-Clé: Transparence, efficacité, ONG, Internet.

Introduction

Non-Governmental organizations (NGOs) in Latin America have been growing in importance mainly as they are being considered crucial social agents for the improvement of democracy (Florez, 1999; Friedman, 2000; Valladares & Neira, 2003; Treviño, 2004), as well as for their role in their fight against poverty and social marginalization (Landim & Thompson, 1997; Friedman, Hochstetler & Clark, 2001; Korzeniewicz & Smith, 2000). However, the recent incidents of corruption in Latin-American NGOs, such as misappropriation of funds and suspicious relation to political parties, have motivated a general distrust toward the compliance of their social goals and the impact of their activities (Vázquez, 2011).

In order to battle corruption within organizations it is essential to eliminate information asymmetry, as organizations strongly need to avoid individual interests, whether they be from managers or workers, placing the interests of the organization on the top (Levine, 2005; Lennerfors, 2007; Halter, Coutinho-Arruda & Halter, 2009). Therefore, a greater transparency to strengthen NGOs legitimacy is needed (Gandía, 2011). Turilli and Floridi (2009), and Lindstedt and Naurin (2010) define transparency as the access to the information about the intentions and behaviors of an organization. According to Lee, Chen and Zhang (2001), Kang and Norton (2004) and Ozcelik (2008), this information should be available to all stakeholders, being the Internet one of the most common communication media to disseminate NGOs information.

NGOs efficiency has turned an important issue to Latin-American Governments, funders and citizens (Brinkerhoff, 2002). Ciborra (2005) considered that disclosure of information via the Internet, or online transparency, not only improves the communication of organizational information but also enhances the efficiency of the organizations results, reduces their costs and improve their competitiveness. Berggren and Bernshteyn (2007), added that internal stakeholders will increase their participation and commitment if there is a greater organizational transparency. Thus, disclosure information promotes organizational trust and its better operability (Burger & Owens, 2010; García-Sánchez, Cuadrado-Ballesteros & Frías-Aceituno, 2012).

The studies that analyze the influence of transparency in NGOs efficiency are scarce (De França, De Figueiredo & Lapa, 2010). Considering that previous studies are focused, mainly, on developed countries (Marcuello, 1999; Golden et al., 2010).

In recent years, NGOs from developing countries are making an effort to improve the transparency of the sector drawing up voluntary accountability mechanisms. Within Latin-American NGOs, Colombian initiatives, such as the code of conduct of "ONG por la transparencia", are remarkable.

This research follows three main objectives. First, the analysis of online transparency by the Colombian NGOs; second, an efficiency analysis of these entities in reaching their social goals; and third, the study of the online transparency effect resulting in a greater efficiency of these NGOs. In order to pursue these objectives, this article is built up as follows: the second section presents an overview of transparency policies carried out by the Latin-American NGOs and previous studies of disclosure of information in NGOs web sites; the third section is focused on the efficiency issue; in the fourth section, the methodologies developed to the objectives of this paper are explained; the fifth, analyzes the results obtained; finally, in the sixth section the main conclusions from this exercise are discussed.

NCOs Transparency Policies and their Disclosure

Vaccaro and Madsen (2009a) pointed out that NGOs should be aware of the importance of transparency policies to guarantee an adequate organizational information access. Likewise, Vaccaro and Madsen (2009b) argued that there are two kinds of transparency: the static and the dynamic. The first one is the most used and is related to unidirectional disclosure of information between the organizations and its stakeholders. The dynamic transparency additionally includes communication among the stakeholders.

In general, in Latin-American countries there is no mandatory legislation that mentions the need for a better transparency in NGOs, as it occurs in other sectors such as listed companies or the public sector. However, there are some exceptions, as shown in Table 1. Additionally, the sector is voluntarily adopting accountability mechanisms drawn up by external agents or by NGOs themselves. Those mechanisms developed by the sector itself are called self-regulation mechanisms and these entities self-regulatory NGOs (Ebrahim, 2003). According to Shea and Sitar (2004), Nelson (2007) and Warren and Lloyd (2009) self-regulation mechanisms can be classified in six categories: certification, rating, award, code of conduct, information service and performance guide (Table 2).

Within the self-regulation mechanisms drawn up by the Latin-American NGOs, it is important to highlight the one developed by the "Centro Virtual para la Transparencia y la Rendición de Cuentas de la Sociedad Civil" (CV Rendir cuentas) in 2010. This organization is made up by 25 self-regulatory NGOs from Latin-America and the Caribbean whose main objective is to enhance the accountability and informative visibility of the sector. Consequently, this mechanism could be considered as an information service, as it discloses relevant information obtained from a standardized form that has to be filled in voluntarily by interested NGOs (Table 3).

Focusing on the Colombian case, there are other self-regulatory mechanisms such as the code of conduct of "ONG por la Transparencia" (ONGxT) drawn up in 2007. The main priority of this organization is to enhance the NGO's transparency, therefore, NGOs interested in being part of this organization need to adopt this code. The compliance of its standards is subject to the disclosure of minimum information provided in the web page of the organization.

The online NGO transparency encompasses the access to information about aspects such as its organizational profile and performance, and its governance and financial management. at the same time, the importance of information inviting stakeholders to participate in the organization of the NGOs is increasing.

According to Greenberg and Macaulay (2009), online transparency of organizational profiles should include the disclosure of information related to organizational history, contact data, agreements with other organizations and information regarding the legal structure of the organization. Ingenhoff and Koelling (2009) and Goatman and Lewis (2007), argued that the number of people that make up the organization should be disseminated. Taylor, Kent and White (2001) and Kang and Norton (2004) stated the need for information regarding the procedures to become affiliated and contribute financially to the organization in order to enhance the involvement of the stakeholders in the organization.

In regards to online disclosure of information about organizational performance, many authors pointed out the relevance of the NGO's mission and vision (Kang & Norton, 2004; Goatman & Lewis, 2007; Waters, 2007). Besides, Waters (2007) and Ingenhoff and Koelling (2009), consider that it is also important to disclose the information related to the organizational strategy, current project and the annual report of activities carried out by an NGO.

In relation to the online dissemination of the NGO governance, Gandía (2011) states that stakeholders should have access to the information about internal rules, minutes, and meetings, as well as the information related to the internal structure and compensations of NGOs Board members.

In keeping with the online dissemination of the organizational financial management, Saxton and Guo (2011) support the publication of audit reports, financial statements, and other data that shows the compliance of the NGOs tax duties. Gandía (2011) also includes the need for publishing NGOs budget, allocation of resources and sources of funding.

Likewise, the online information that promotes the participation of internal and external stakeholders in the organization is increasingly considered; specially the aspects related to receiving and handling complaints and enquires (Goatman & Lewis, 2007), the disclosure of documentation (bibliography and video) that let stakeholders learn more about the organization's mission (Taylor, Kent & White, 2001), and the information about the procedures to evaluate NGOs projects (Waters, 2007).

NCOs Efficiency

Efficiency is defined as the rational use of resources in order to maximize benefits (García-Sánchez, 2010). Due to the non-profit-making characteristic of the NGOs sector, efficiency should not be perceived as the maximization of benefits but as the achievement of social goals (Marcuello, 1999). At this point, Epstein and McFarlan (2011) claim that NGOs efficiency must be based on the improvement of the society welfare.

Transparency is increasingly considered a mechanism to improve organizations efficiency, therefore, it promotes the organization trust and its competitiveness since it enables better governance and reduces agency costs (Boot & Thakor, 2001; Xuegang, 2004; Chen & Hasan, 2006; Pasiouras, 2008; Zhongsheng & Hanwen, 2008; Wu & Zang, 2009; Refait-Alexandre, Farvaque & Weill, 2011).

Despite the fact that most of the studies analyzing the influence of transparency in a greater efficiency are focused on lucrative entities, De Castro (2005) considers that the disclosure of information promotes the NGOs fundraising, which is crucial for the running of the organization and the fulfillment of its social goals. In addition, De França et al. (2010) argued that transparency reduces the information asymmetry caused by conflicts of interests between NGOs managers and their main stakeholders (beneficiaries and benefactors). In this line, Burger and Owens (2010) noted that the disclosure of information is very important to control the performance of these entities.

In order to calculate efficiency, Golden et al. (2012) manifest that the use of financial ratios could yield subjective and tampering results. Epstein and McFarlan (2011), add that an adequate assessment of NGOs efficiency involves obtaining financial and non-financial information about the resources (input) and the results (output) of the organization.

The literature about NGOs efficiency consider as inputs those operational cost (Harrison & Sexton, 2006; Alexander, Haug & Jaforullah, 2010) the contributions received by the organization (Golden et al., 2012) and the number of employees (Alexander et al., 2010). Among the analyzed outputs the following are to be included: Total income, total number of projects carried out (García & Marcuello, 2002), and total investment in projects (Golden et al., 2012).

Alexander et al. (2010), pointed out that not only is important to analyze organizational efficiency, but also to study those factors affecting it. According to this, diverse factors such as organizational age (Marudas & Jacobs, 2007), size (Marcuello, 1999; Alexander, Haug & Jaforullah, 2010), and legal structure (García & Marcuello, 2002) must be considered. Additionally, Gutiérrez-Nieto, Serrano-Cinca and Mar-Molinero (2009), noted that transparency is a factor that improves efficiency in getting the social objectives of some non-profit entities.

Methodology

Analysis of Online Transparency: Disclosure Index

To fulfill the first objective of this study an online transparency index (TI) has been developed, following previous works by Verbruggen, Christiaens and Millis (2011), and Saxton and Guo (2011).

Items selections of TI are based on the 61 items indicated in Table 3. This general index has been made up by the following five partial indexes: i) online transparency of organizational profile (TIPf); ii) online transparency of organizational performance (TIPe); iii) online transparency of organizational governance (TIGov); iv) online transparency of financial management (TIF); and v) online transparency on stakeholder's participation (TIPar).

Each partial index (TIJ) is determined by the relation of total sum of items identified in the web page (tii) and the total number of items that form part of the partial index. In order to express this in percentage it was multiplied by 100.

Due to the lack of clear empirical evidence on the importance of the items and sections that compose our online transparency index, we decided to assess them with an identical weight in line with the methodology proposed by Rodríguez (2004), Verbrugen et al. (2011), and Saxton and Guo (2011). In the same way, in order to assign a score to the items, if the item appears in the web page it is assigned a score of 1, if it does not it is assigned a score of 0; therefore, the TI index would be calculated under the following expression:

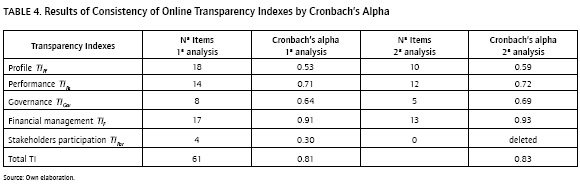

Then, a consistency analysis of the index and partial indexes was carried out based on Cronbach's alpha coefficient, in line with Gandía (2011), and Saxton and Guo (2011). Taken into consideration the minimum levels of reliability indicated by Nunnally (1978), the consistency index TI was especially good (0.81), as shown in Table 4. However, consistency levels of the partial indexes were heterogeneous; specially, the consistency level of TIPf which was low, acceptable to TIPe, moderate to TIGov and very good to ITF. TIPor had an inconsistent reliability. Besides, TIPor was rejected and some items of the other partial indexes were also deleted in order to increase their consistency. Therefore, the TI index was drawn up by 39 items and divided into 4 partial indexes (Appendix) following this expression:

Efficiency Analysis: DEA

Regarding the second objective of this paper, the analysis of NGO efficiency, Data Envelopment Analysis (DEA) has been used. This methodology is the most suitable to analyze non-profit organizations (De França et al., 2010). Particularly, it is used by the sector to analyze NGOs efficiency in achieving their social objectives (Marcuello, 1999; Golden et al., 2012), and NGOs efficiency in fun-draising capacity (García & Marcuello, 2003; Marudas & Jacobs, 2010). Moreover, DEA is also used to analyze the efficiency of good governance practices of listed companies (García-Sánchez, 2010) and banks (Refait-Alexandre et al., 2011).

In this study the efficiency of Colombian NGOs to reach their social goals is analyzed. A selection of variable inputs and outputs has been taken based on the literature previously reviewed and, taken into consideration the kind of efficiency that we are analyzing (Table 5).

Regarding the characteristics of DEA, it is a non-parametric method developed by Farrel (1957). It mainly consists on linear programming techniques to empirically obtain a best practice production frontier and evaluate efficiencies of a set of similar organizations or Decision Making Units (DMUs). Thus, the most efficient DMUs are those that produce with a minimum of inputs obtained the desired outputs (input-oriented) or those that maximize outputs with the available inputs (output-oriented). Considering any of these methodologies (input orientated or output orientated), an organization would be technically efficient when it obtains a score of 1.

An extension to Farrell's work (1957) is a model assuming the constant return to a scale that was developed by Charnes, Cooper and Rhodes (1978). Later on, Banker, Charnes and Cooper (1984), developed a model that added a restriction on the convexity assumption (N1'λ = 1) to the former model, indicating the variable return to the scale (RVS). This restriction avoids the comparison between DMUs with any different size. Additionally, Simar and Wilson (2002a) suggested the use of bootstrapping techniques in order to consider the sampling noise in the resulting efficiency estimators, maintaining the statistical properties of DEA estimators. According to this, current studies recommend the analysis of efficiency with RVS and bootstrapping techniques (Garcia-Sanchez, 2010). Therefore, in this work we have calculated efficiency by VRS together with bootstrapping techniques and with output orientation as it is showed in the following expression:

Where:

Y: matrix output m x n

X: matrix input k x n

θ: is scalar score and multiple output vector

λ: is a Nx1 vector constant. This multiples inputs matrix and outputs matrix.

N: number of DMU

N1: Nx1 vector of ones

In order to estimate efficiency we have used Wilson's software package for Frontier Efficiency Analysis with R (FEAR).

Transparency Analysis versus Efficiency: Empirical Analysis

In this section a close analysis of the online transparency influence in Colombian NGOs efficiency will be estimated by the so-called truncated regression method. This methodology is appropriate for data analysis ranging from 0 to 1 distribution (Jacobs, Smith & Street, 2006). Results by Simar and Wilson (2007), showed that it provides a better statistical inference than Tobit regression does. Nevertheless, this approach may be inconsistent unless the estimates DEA efficiency scores are corrected by a bootstrapping procedure. Bearing this in mind, our procedure applied in the present study follows the bootstrap approach developed by Simar and Wilson (1998, 2000b).

Moreover, truncated regression methodology is used in recent works related to non-profit organizations (Biener & Martin, 2011) and those which analyze the transparency as an explicative factor of organization efficiency (Refait-Alexandre et al, 2011).

Then, assuming that θi has a being distributed based upon a set of m ≥ n normally distributed random variables ∂;, j = 1.....m and zi, each corresponding vector of the global transparency index and the partial indexed that compose it. The truncated regression will be calculated following this expression:

Where  J refers to a vector of covariates, β represent the parameter vector and εj is a normally distributed error term. On this basis θ,.....θn is defined as a truncated set of ∂i,......∂n, with ∂j ≤ 1 and Zi = J, for θ, = ∂j.

J refers to a vector of covariates, β represent the parameter vector and εj is a normally distributed error term. On this basis θ,.....θn is defined as a truncated set of ∂i,......∂n, with ∂j ≤ 1 and Zi = J, for θ, = ∂j.

The analysis of associations through independent variables was done using Pearson Correlation Coefficient, in line with Pasiouras (2008). We used Wilson's software package for Frontier Efficiency Analysis with R (FEAR) to bootstrapping procedure and, Stata program version 11.1 to estimate truncated regression and correlation analysis.

Sphere of Study

In order to perform the research objectives of this paper, the 400 Latin American NGOs that appear on the online platform "Centro Virtual para la Transparencia y la Rendición de Cuentas de la Sociedad Civil" (CV Rendir cuentas) were analyzed. However, some of the population selected could not be examined either because their web pages were under construction, not available, did not have a website or were nonexistent. Therefore, the final sample was 196 organizations. The analysis period was April to May 2013.

Regarding the characteristics of the final sample, it is worth mentioning that it was mainly made up by entities from Bogota, the most populous city in the country, and the most populous cities of Antioquia, followed by cities from the Caribbean Coast, Caldas and, to a lesser extent, Santander and Quindio. With the exception of Quindio, the workforce of the organizations sampled were mainly made up of salaried staff. In addition, the sample performs from four to twelve projects per year with a social impact between 1,866 and 16,928 beneficiaries. Likewise, the entities selected converged in having greater financial support from public funding than other agencies of international cooperation.

Focusing on the above characteristics by city, it is observed that Bogota and the total for Antioquia exhibited the largest number of salaried staff, while the NGOs from Quindio and Santander had a greater number of volunteers. In addition, Bogota and Antioquia also lead the group, based on the total number of projects and the number of beneficiaries. In addition, entities from Santander enjoyed the greatest support from agencies of international cooperation, whereas those from Quindio were principally funded by public entities (Table 6).

Results

Results of the Online Transparency Index

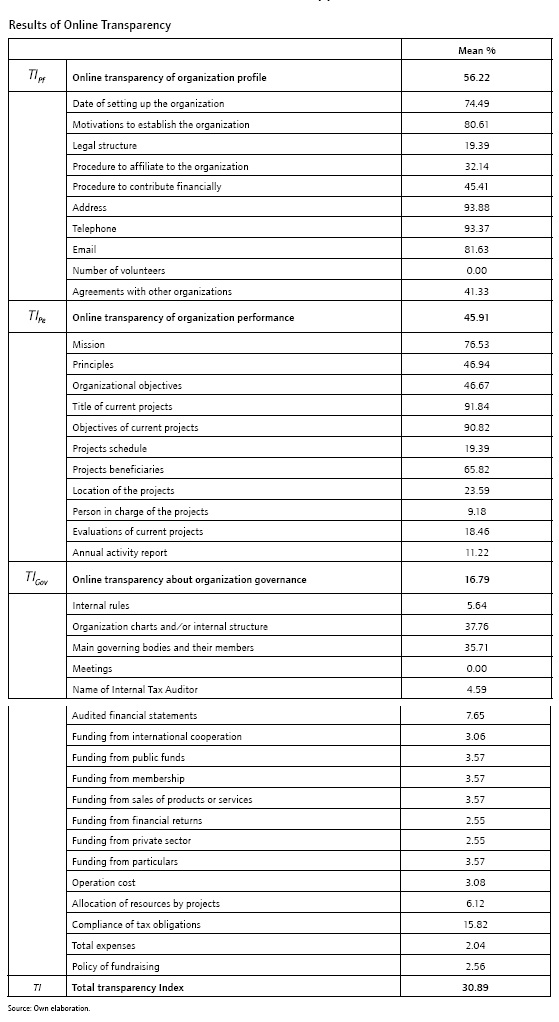

The results show that in general terms, the level of online information disclosure among the Colombian NGOs is low. In particular, less than 31% of the total items that compose the Transparency Index (TI) are published in the websites of these entities. Therefore, it seems that Colombian entities are in line with the scarce importance that NGOs from other countries, such as Switzerland (Ingenhoff & Koelling, 2007) and the United States (Kang & Norton, 2004) give to online transparency. The information most disseminated is that related to the organizational profile and performance. There is significantly less information published regarding their governance, with the information regarding financial management being very limited (Table 7).

Delving further in each of the partial indexes it is observed that, with regards to online information about their profile, all the organizations supplied their address, telephone number and email address. Likewise, Colombian NGOs are quite prone to justifying the motivations for creating their organization. On the contrary, few entities present online visibility with regards to information about how to affiliate to the organization or the legal structure. Additionally, in none of the cases analyzed was found information concerning the volunteers of the organization (Appendix).

In relation to online information access of the organizational performance, the online visibility regarding the title and objectives of current projects is noteworthy. Moreover, it is quite common to disclose the mission and information related to the beneficiaries of the projects. Nevertheless, the online dissemination of the annual report is surprisingly low. Likewise, in very few of the cases analyzed information about the person in charge of the projects was published.

Related to the online transparency of the organizations' performance, almost 40% of the NGOs analyzed published an organizational chart on their web pages. To a lesser extent, main governing bodies and their members is disseminated. Moreover, the dissemination of the internal rules and name of Internal Tax Auditor is very limited and online disclosure of meetings was nonexistent.

Despite the fact that the online transparency of the financial management is quite low, it is worth noting that the documents that serve to prove compliance with the tax obligations is the information most disclosed in this manner, reaching near 16% of the cases analyzed. The next information most available in their web pages is the audited financial statements and the allocation of resources by project, albeit with a 7.65% and 6.12% respectively. The remaining items do not surpass 4%, indicating the clear lack of transparency regarding the financial issues of the organization.

Looking at Table 7, the NGOs of all regions converge in the greater dissemination of two of the transparency dimensions related to the profile and the performance of the organization. However, regarding the level of online transparency, NGOs located in Bogota show the highest level of online transparency, while the NGOs from the Caribbean Coast are those that make the least use of the web pages as a strategic communication channel.

Finally, the top 10 transparent NGOs are from Bogota, Antioquia and the Caribbean Coast with levels of up to 65%. If we compare these results with the transparency index (TI) by regions, we can observe a moderate difference. In the case of Bogota, the most transparent NGOs surpassed the TI of their region in 39.76% .There is a difference of 36.99% and 35.47% in the case of Antioquia and Caldas (Table 8).

Results of the Efficiency Analysis

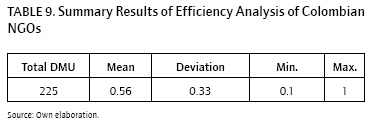

The Colombian NGOs reach, in general terms, a level of efficiency of 0.56 points as it is indicated in Table 9. From the 196 NGOs analyzed just 33 are efficient representing a 16.83% of the sample.

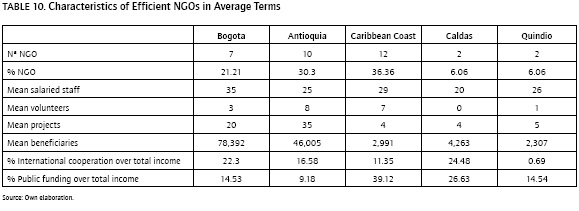

In average terms, there are six volunteers working with each of the efficient NGOs. Their percentage of public funding is lower compared to the mean of all NGOs analyzed. In contrast to this, efficient NGOs receive a higher percentage of international cooperation funding (Table 10).

The efficient NGOs come mainly from the region of Bogota with a 33.33%, followed by the Caribbean Coast NGOs and Antioquia with 30.30% and 24.24%, respectively. In the same way, results indicate one efficient NGO from Caldas and two efficient NGOs from Santander.

By analyzing the characteristics of efficient NGOs it is observed that most of them work with less salaried staff than the other NGOs analyzed for their region. It is also worth noting that most of efficient NGOs work with less volunteers than the mean of the NGOs of its region, except in the case of Antioquia and the Caribbean Coast. Efficient NGOs from Bogota and Antioquia are the only ones that indicate a number of projects that is above the average for its region, showing a higher volume of beneficiaries than the rest of its region partners.

With the exception of NGOs from the department of Antioquia, all the efficient organizations studied show a higher percentage of funding provided by international cooperation than the rest of the organizations in their region. NGOs from the Caribbean Coast are the only ones that receive a higher public funding than the average of its region (Table 10).

Results of Empirical Analysis

Following the methodology above mentioned, Table 11 presents the Pearson Correlation Coefficient for all the independent variables included in the model. Results indicate that TI has a correlation with almost all of the other variables. In order to avoid multi-collinearity problems, we decided not to consider the global transparency index and maintain all the partial indexes that compose it.

Following the results in Table 12, the expected influence of the online transparency of performance (TIPe) in a greater efficiency is confirmed (p < 0.1). Besides, there is a strong relation between the online transparency of financial aspects (TIF) and its efficiency (p < 0.01). This result is similar to the research by Chen and Hasan (2006) in banks.

The effect of governance over online transparency (TIGov) in Colombian NGOs efficiency was neutral, not coinciding with the positive evidence showed by Refait-Alexandre et al. (2011) in the bank sector. Likewise, we cannot confirm that there is statistical significant relation between online transparency of organization's profile and its efficiency.

A comparative analysis of the level of the online transparency between the efficient of NGOs and the rest of the sample is shown in Table 13. In general, it is highlighted that efficient entities present better results than the other NGOs, both in general terms and almost all of the partial indexes.

Conclusions

In recent years, activities of Latin-American NGOs have increased considerably. However, the high level of corruption in those countries has undermined the legitimacy of the sector. As a consequence Latin-American society distrusts the efficiency of these entities in complying with its social commitments. As it is mentioned above, informative transparency is one of the main mechanisms that prevents corruption and enhances a better way of working by organizations. Nowadays, Internet could be considered a strategic tool to disseminate information.

The self-regulation mechanisms of Latin-American NGOs and specially those from Colombia, are part of the initiatives that the sector is carrying out to improve the information access of the organization. This paper pursued the analysis of the online transparency of Colombian NGOs, as well as the analysis of the efficiency of these entities in order to reach their social goals and of the online transparency influence resulting in a better efficiency of Colombian NGOs.

Less than half of the studied NGOs had a web page available, indicating that the awareness of the Internet as a useful communication element is scarce. Furthermore, there is a low level of online transparency comparing to the results of such organizations from other geographical areas.

The information disclose is mainly focused on the organization profile followed by their performance. Online access to information related to the mechanism of the organization and the financial management is very limited.

Colombian NGOs reach slightly more than half of the social objectives that they should execute. This efficiency could be considered as moderate in contrast to the results of previous studies in other European countries (García & Marcuello, 2003; Golden et al, 2012). In this regard, more effort is needed in the management of the organization in order to obtain a stronger impact of their activities. Coming back to the general characteristics of efficient NGOs, these organizations mainly work with salaried staff and low levels of public funding. However, they receive a higher level of international cooperation funding compared to the other Colombian NGOs studied.

Our findings about transparency effects in NGOs efficiency showed that online disclosure of performance and financial management information contributes to a greater efficiency of the organizations. According to Agency Theory, this result could be due to the use of Internet as an accountability mechanism of the activities that NGOs carry out, reducing stakeholders distrust in the development of their projects and, therefore, in the final accomplishment of their social objectives. In the same way, the disclosure of financial data may avoid corruption in the organization, ensuring a better management of the resources.

Finally, this paper not only contributes to enhance the use of websites to communicate information, but also to a better understanding of the contents that embrace an adequate online transparency. NGOs could then respond better to the information needs of their stakeholders. Furthermore, this paper demonstrates the usefulness of disclosing information on the Internet as a mechanism for optimizing the resources of the organization and thus strengthening their legitimacy as agents that serve society.

References

Alexander, W. R. J., Haug, A. A., & Jaforullah, M. (2010). A two-stage double-bootstrap data envelopment analysis of efficiency differences of New Zealand secondary schools. Journal of Productivity Analysis, 34(2), 99-110.

Banker, R. D., Charnes, A., & Cooper, W. W. (1984). Some models for estimating technical and scale inefficiencies in data envelopment analysis. Management Science, 30(9), 1078-1092.

Berggren, E., & Bernshteyn, R. (2007). Organizational transparency drives company performance. The Journal of Management Development, 26(5), 411-417.

Biener, C., & Martin, E. (2011). The performance of microinsurance programs: a data envelopment. Journal of Risk and Insurance, 78(1), 83-115.

Boot, A. W. A., & Thakor, A. V. (2001). The many faces of information disclosure. The Review of Financial Studies, 14(4), 1021-1057.

Brinkerhoff, J. M. (2002). Government-nonprofit partnership: A defining framework. Public Administration and Development, 22(1), 19-30.

Burger, R., & Owens, T. (2010). Promoting transparency in the NGO sector: Examining the availability and reliability of self-reported data. World Development, 38(9), 1263-1277.

Charnes, A., Cooper, W. W., & Rhodes, E. (1978). Measuring the Efficiency of Decision Making Units. European Journal of Operational Research, 2(6), 429-444.

Chen, Y, & Hasan, I. (2006). The transparency of the banking system and the efficiency of information-based bank runs. Journal of Financial Intermediation, 15, 307-331.

Ciborra, C. (2005). Interpreting e-government and development: Efficiency, transparency or governance at a distance? Information Technology & People, 18(3), 260-279.

De Castro Sanz, M. (2005). La Responsabilidad Social de las Empresas, o un nuevo concepto de empresa. CIRIEC-España, Revista de Economía Pública, Social y Cooperativa, 53, 29-51.

De França, J. M. F., De Figueiredo, J. N., & Lapa, J. S. (2010). A DEA methodology to evaluate the impact of information asymmetry on the efficiency of not-for-profit organizations with an application to higher education in Brazil. Annals of Operations Research, 173(1), 39-56.

Ebrahim, A. (2003). Accountability in Practice: Mechanisms for NGOs. World Development, 31(5), 813-829.

Epstein, M. J., & McFarlan, F. W. (2011). Measuring the efficiency and effectiveness of a nonprofit's performance. Strategic Finance, 93(4), 27-34.

Farrell, M. J. (1957). The measurement of productive efficiency. Journal of the Royal Statistical Society, Series A, 120(3), 253-290.

Florez, M. (1997). Non-governmental organisations and philanthropy: the Colombian case. Voluntas, 8(4), 386-400.

Friedman, E. J. (2000). Unfinished Transitions, Women and the Gendered Development of Democracy in Venezuela, 1936-1996. University Park: Penn State University Press.

Friedman, E. J., Hochstetler, K., & Clark, A. M. (2001). Sovereign limits and regional opportunities for global civil society in Latin America. Latin American Research Review, 36(3), 7-35.

Gandía, J. L. (2011). Internet disclosure by nonprofit organizations: Empirical evidence of nongovernmental organizations for development in Spain. Nonprofit and Voluntary Sector Quarterly, 40(1), 57-58.

García, L. I., & Marcuello, C. (2002). Eficiencia y captación de fondos en las organizaciones no gubernamentales para el desarrollo. Ciriec-España, Revista de Economía Pública, Social y Cooperativa, 58, 221-249.

García-Sánchez, I. M. (2010). The effectiveness of corporate governance: Board structure and business technical efficiency in Spain. Central European Journal of Operations Research, 18(3), 311-339.

García-Sánchez, I. M., Cuadrado-Ballesteros, B., & Frías-Aceituno, J. (2012). Determinants of E-Government Development: Some Methodological Issues. Journal of Management and Strategy, 3(3), 11-20.

Goatman, A. K., & Lewis, B. R. (2007). Charity E-volution? An evaluation of the attitudes of UK charities towards website adoption and use. International Journal of Nonprofit and Voluntary Sector Marketing, 12(1), 33-46.

Golden, L. L., Brockett, P. L., Betak, J. F., Smith, K. H., & Cooper, W. (2012). Efficiency metrics for nonprofit marketing/fundraising and service provision a DEA analysis. Journal of Management and Marketing Research, 9(1), 1-25.

Greenberg, J., & MacAulay, M. (2009). NPO 2.0? Exploring the web presence of environmental nonprofit organizations in Canada. Global Media Journal, 2(1), 63-88.

Gutiérrez-Nieto, B., Serrano-Cinca, C., & Mar-Molinero, C. (2007). Micro-finance institutions and efficiency. Omega, 35(2), 131-142.

Gutiérrez-Nieto, B., Serrano-Cinca, C., & Mar-Molinero, C. (2009). Social efficiency in microfinance institutions. The Journal of the Operational Research Society, 60(1), 104-119.

Halter, M. V., Coutinho-Arruda, M. C., & Halter, R. B. (2009). Transparency to Reduce Corruption? Journal of Business Ethics, 84(3), 373-385.

Harrison, J. P., & Sexton, C. (2006). The improving efficiency frontier of religious not-for profit hospitals. Hospital Topics, 84(1), 2-10.

Ingenhoff, D., & Koelling, A. M. (2009). The potential of web sites as a relationship building tool for charitable fundraising NPOs. Public Relations Review, 35(1), 66-77.

Jacobs, R., Smith, P. C., & Street, A. (2006). Measuring efficiency in health care: analytic techniques and health policy. Cambridge, MA: Cambridge University Press.

Kang, S., & Norton, H. E. (2004). Nonprofit organizations' use of the World Wide Web: Are they sufficiently fulfilling organizational goals? Public Relations Review, 30(3), 279-284.

Korzeniewicz, R. P., & Smith, W. C. (2000). Poverty, inequality, and growth in Latin America: Searching for the high road to globalization. Latin American Research Review, 35(3), 7-54.

Landim L., & Thompson A. (1997). Non-governmental organisations and philanthropy in Latin America: an overview. Voluntas, 8(4),337-350.

Lee, T. D., Chen, J. Q., & Zhang, R. (2001). Utilizing the Internet as a competitive tool for non-profit organizations. The Journal of Computer Information Systems, 41(3), 26-31.

Lennerfors, T. T. (2007). The transformation of transparency on the act on public procurement and the right to appeal in the context of the war on corruption. Journal of Business Ethics, 73(4), 381-390.

Levine, D. P. (2005). The corrupt organization. Human Relations, 58(6), 723-739.

Lindstedt, C., & Naurin, D. (2010). Transparency is not enough: Making transparency effective in reducing corruption. International Political Science Review, 37(3), 301-322.

Marcuello, C. (1999). Análisis de la conducta de la eficiencia de las organizaciones no gubernamentales españolas. Economía y Cooperación al Desarrollo, 778, 181-196.

Marudas, N. P., & Jacobs, F. A. (2007). The extent of excessive or insufficient fundraising among US arts organizations and the effect of organizational efficiency on donations to US arts organizations. International Journal of Nonprofit and Voluntary Sector Marketing, 72(3), 267-273.

Nelson, J. (2007). The Operation of Non-Governmental Organizations (NGOs) in a World of Corporate and Other Codes of Conduct. Corporate Social Responsability Iniciative. Working Paper No. 34, Cambridge, MA: John F. Kennedy School of Government, University of Harvard. Retrieved on January 2012 from: http://www. hks.harvard.edu/mrcbg/CSRI/publications/workingpaper_34_ nelson.pdf.

Nunnally. J. C. (1978). Psychometric Theory 2nd ed. McGraw-Hill: Nueva York, USA.

Ozcelik, Y. (2008). Globalization and the Internet: Digitizing the nonprofit sector. Journal of Global Business Issues, 2(1), 149-152.

Pasiouras, F. (2008). International evidence on the impact of regulations and supervision on banks' technical efficiency: An application of two-stage data envelopment analysis. Review of Quantitative Finance and Accounting, 30(2), 187-223.

Refait-Alexandre, C., Farvaque, E., & Weill, L. (2011). Are Transparent Banks More Efficient? Evidence from Russia. Retrieved on January 2012 from SSRN: http://ssrn.com/abstract=1792605 or https://doi.org/10.2139/ssrn.1792605.

Saxton, G. D., & Guo, C. (2011). Accountability online: Understanding the web-based accountability practices of nonprofit organizations. Nonprofit and Voluntary Sector Quarterly, 40(2), 270-295.

Schepers, D. H. (2006). The impact of NGO network conflict on the corporate social responsibility strategies of multinational corporations. Business and Society, 45(3), 282-299.

Shea, C., & Sitar, S. (2004). NGO Accreditation and Certification: The Way Forward? An Evaluation of the Development Community's Experience. Institutional Center for Not for profit Law. Washington. Retrieved on January 2012 from: http://www.usaid.gov/our_work/crosscutting_programs/private_voluntary_coopera-tion/conf_icnl.pdf.

Simar, L., & Wilson, P. (1998). Sensitivity analysis of efficiency scores: how to bootstrap in non-parametric frontier models. Management Science, 44, 49-61.

Simar, L., & Wilson P. (2000a). Statistical inference in nonparame-tric frontier models: the state of the art. Journal of Productivity Analysis, 73(1), 49-78.

Simar, L., & Wilson, P. (2000b). A general methodology for bootstrapping in nonparametric frontier models. Journal of applied statistics, 27(6), 779-802.

Simar, L., & Wilson, P. (2007). Estimation and inference in two-stage, semi-parametric models of production processes. Journal of Econometrics, 736(1), 31-64.

Taylor M., Kent, M. L., & White, W. J. (2001). How activist organizations are using the Internet to build relationships. Public Relations Review, 27(3), 263-284.

Treviño, J. (2004). Las ONG de derechos humanos y la redención de la soberanía del estado mexicano. Foro Internacional, 777(3), 509-539.

Turilli, M., & Floridi, L. (2009). The ethics of information transparency. Ethics and Information Technology, 77(2), 105-112.

Vaccaro, A., & Madsen, P. (2009a). Corporate dynamic transparency: The new ICT-driven ethics? Ethics and Information Technology, 77 (2), 113-122.

Vaccaro, A., & Madsen, P. (2009b). ICT and an NGO: Difficulties in attempting to be extremely transparent. Ethics and Information Technology 77 (3), 221-23.

Valladares, A. M., & Neira, I. (2003). Impacto de la ayuda oficial al desarrollo en Centroamérica. Estudios Económicos de Desarrollo Internacional, 3(1), 1-19.

Vázquez, J. J. (2011). Attitudes toward nongovernmental organizations in Central America. Nonprofit and Voluntary Sector Quarterly, 40(1), 166-184.

Verbruggen, S., Christiaens, J., & Milis, K. (2011). Can resource dependence and coercive isomorphism explain nonprofit organizations' compliance with reporting standards? Nonprofit and Voluntary Sector Quarterly, 40(1), 5-32.

Warren, S., & Lloyd, R. (2009). Civil Society Self-Regulation: The Global Picture. (Briefing Paper No. 119). One World Trust, London. Retrieved on January 2012 from: http://www.oneworldtrust.org/index.php?option=com_docman&task=doc_view&gid=377&tmpl=component&format=raw&Itemid=55.

Waters, R. D. (2007). Nonprofit organizations' use of the Internet: A content analysis of communication trends on the Internet sites of the philanthropy 400. Nonprofit Management and Leadership, 78(1), 59-76.

Wu, I. X., & Zang, J. S. (2009). The Voluntary Adoption of Internationally Recognized Accounting Standards and Firm Internal Performance Evaluation. The Accounting Review, 84(4), 1281-1310.

Xuegang, C. (2004). The Effects of Corporate Governance on Corporate Transparency Experience from China Listed Companies. Accounting Research, 8, 72-80.

Zhongsheng, Z., & Hanwen, C. (2008). Accounting Information Transparency and Resources Allocation Efficiency: Theory and Empirical Evidence. Accounting Research, 12, 56-62.

Appendix

Referencias

Alexander, W. R. J., Haug, A. A., & Jaforullah, M. (2010). A two-stage double-bootstrap data envelopment analysis of efficiency differences of New Zealand secondary schools. Journal of Productivity Analysis, 34(2), 99-110.

Banker, R. D., Charnes, A., & Cooper, W. W. (1984). Some models for estimating technical and scale inefficiencies in data envelopment analysis. Management Science, 30(9), 1078-1092.

Berggren, E., & Bernshteyn, R. (2007). Organizational transparency drives company performance. The Journal of Management Development, 26(5), 411-417.

Biener, C., & Martin, E. (2011). The performance of microinsurance programs: a data envelopment. Journal of Risk and Insurance, 78(1), 83-115.

Boot, A. W. A., & Thakor, A. V. (2001). The many faces of information disclosure. The Review of Financial Studies, 14(4), 1021-1057.

Brinkerhoff, J. M. (2002). Government-nonprofit partnership: A defining framework. Public Administration and Development, 22(1), 19-30.

Burger, R., & Owens, T. (2010). Promoting transparency in the NGO sector: Examining the availability and reliability of self-reported data. World Development, 38(9), 1263-1277.

Charnes, A., Cooper, W. W., & Rhodes, E. (1978). Measuring the Efficiency of Decision Making Units. European Journal of Operational Research, 2(6), 429-444.

Chen, Y, & Hasan, I. (2006). The transparency of the banking system and the efficiency of information-based bank runs. Journal of Financial Intermediation, 15, 307-331.

Ciborra, C. (2005). Interpreting e-government and development: Efficiency, transparency or governance at a distance? Information Technology & People, 18(3), 260-279.

De Castro Sanz, M. (2005). La Responsabilidad Social de las Empresas, o un nuevo concepto de empresa. CIRIEC-España, Revista de Economía Pública, Social y Cooperativa, 53, 29-51.

De França, J. M. F., De Figueiredo, J. N., & Lapa, J. S. (2010). A DEA methodology to evaluate the impact of information asymmetry on the efficiency of not-for-profit organizations with an application to higher education in Brazil. Annals of Operations Research, 173(1), 39-56.

Ebrahim, A. (2003). Accountability in Practice: Mechanisms for NGOs. World Development, 31(5), 813-829.

Epstein, M. J., & McFarlan, F. W. (2011). Measuring the efficiency and effectiveness of a nonprofit's performance. Strategic Finance, 93(4), 27-34.

Farrell, M. J. (1957). The measurement of productive efficiency. Journal of the Royal Statistical Society, Series A, 120(3), 253-290.

Florez, M. (1997). Non-governmental organisations and philanthropy: the Colombian case. Voluntas, 8(4), 386-400.

Friedman, E. J. (2000). Unfinished Transitions, Women and the Gendered Development of Democracy in Venezuela, 1936-1996. University Park: Penn State University Press.

Friedman, E. J., Hochstetler, K., & Clark, A. M. (2001). Sovereign limits and regional opportunities for global civil society in Latin America. Latin American Research Review, 36(3), 7-35.

Gandía, J. L. (2011). Internet disclosure by nonprofit organizations: Empirical evidence of nongovernmental organizations for development in Spain. Nonprofit and Voluntary Sector Quarterly, 40(1), 57-58.

García, L. I., & Marcuello, C. (2002). Eficiencia y captación de fondos en las organizaciones no gubernamentales para el desarrollo. Ciriec-España, Revista de Economía Pública, Social y Cooperativa, 58, 221-249.

García-Sánchez, I. M. (2010). The effectiveness of corporate governance: Board structure and business technical efficiency in Spain. Central European Journal of Operations Research, 18(3), 311-339.

García-Sánchez, I. M., Cuadrado-Ballesteros, B., & Frías-Aceituno, J. (2012). Determinants of E-Government Development: Some Methodological Issues. Journal of Management and Strategy, 3(3), 11-20.

Goatman, A. K., & Lewis, B. R. (2007). Charity E-volution? An evaluation of the attitudes of UK charities towards website adoption and use. International Journal of Nonprofit and Voluntary Sector Marketing, 12(1), 33-46.

Golden, L. L., Brockett, P. L., Betak, J. F., Smith, K. H., & Cooper, W. (2012). Efficiency metrics for nonprofit marketing/fundraising and service provision a DEA analysis. Journal of Management and Marketing Research, 9(1), 1-25.

Greenberg, J., & MacAulay, M. (2009). NPO 2.0? Exploring the web presence of environmental nonprofit organizations in Canada. Global Media Journal, 2(1), 63-88.

Gutiérrez-Nieto, B., Serrano-Cinca, C., & Mar-Molinero, C. (2007). Micro-finance institutions and efficiency. Omega, 35(2), 131-142.

Gutiérrez-Nieto, B., Serrano-Cinca, C., & Mar-Molinero, C. (2009). Social efficiency in microfinance institutions. The Journal of the Operational Research Society, 60(1), 104-119.

Halter, M. V., Coutinho-Arruda, M. C., & Halter, R. B. (2009). Transparency to Reduce Corruption? Journal of Business Ethics, 84(3), 373-385.

Harrison, J. P., & Sexton, C. (2006). The improving efficiency frontier of religious not-for profit hospitals. Hospital Topics, 84(1), 2-10.

Ingenhoff, D., & Koelling, A. M. (2009). The potential of web sites as a relationship building tool for charitable fundraising NPOs. Public Relations Review, 35(1), 66-77.

Jacobs, R., Smith, P. C., & Street, A. (2006). Measuring efficiency in health care: analytic techniques and health policy. Cambridge, MA: Cambridge University Press.

Kang, S., & Norton, H. E. (2004). Nonprofit organizations' use of the World Wide Web: Are they sufficiently fulfilling organizational goals? Public Relations Review, 30(3), 279-284.

Korzeniewicz, R. P., & Smith, W. C. (2000). Poverty, inequality, and growth in Latin America: Searching for the high road to globalization. Latin American Research Review, 35(3), 7-54.

Landim L., & Thompson A. (1997). Non-governmental organisations and philanthropy in Latin America: an overview. Voluntas, 8(4),337-350.

Lee, T. D., Chen, J. Q., & Zhang, R. (2001). Utilizing the Internet as a competitive tool for non-profit organizations. The Journal of Computer Information Systems, 41(3), 26-31.

Lennerfors, T. T. (2007). The transformation of transparency on the act on public procurement and the right to appeal in the context of the war on corruption. Journal of Business Ethics, 73(4), 381-390.

Levine, D. P. (2005). The corrupt organization. Human Relations, 58(6), 723-739.

Lindstedt, C., & Naurin, D. (2010). Transparency is not enough: Making transparency effective in reducing corruption. International Political Science Review, 37(3), 301-322.

Marcuello, C. (1999). Análisis de la conducta de la eficiencia de las organizaciones no gubernamentales españolas. Economía y Cooperación al Desarrollo, 778, 181-196.

Marudas, N. P., & Jacobs, F. A. (2007). The extent of excessive or insufficient fundraising among US arts organizations and the effect of organizational efficiency on donations to US arts organizations. International Journal of Nonprofit and Voluntary Sector Marketing, 72(3), 267-273.

Nelson, J. (2007). The Operation of Non-Governmental Organizations (NGOs) in a World of Corporate and Other Codes of Conduct. Corporate Social Responsability Iniciative. Working Paper No. 34, Cambridge, MA: John F. Kennedy School of Government, University of Harvard. Retrieved on January 2012 from: http://www. hks.harvard.edu/mrcbg/CSRI/publications/workingpaper_34_ nelson.pdf.

Nunnally. J. C. (1978). Psychometric Theory 2nd ed. McGraw-Hill: Nueva York, USA.

Ozcelik, Y. (2008). Globalization and the Internet: Digitizing the nonprofit sector. Journal of Global Business Issues, 2(1), 149-152.

Pasiouras, F. (2008). International evidence on the impact of regulations and supervision on banks' technical efficiency: An application of two-stage data envelopment analysis. Review of Quantitative Finance and Accounting, 30(2), 187-223.

Refait-Alexandre, C., Farvaque, E., & Weill, L. (2011). Are Transparent Banks More Efficient? Evidence from Russia. Retrieved on January 2012 from SSRN: http://ssrn.com/abstract=1792605 or https://doi.org/10.2139/ssrn.1792605.

Saxton, G. D., & Guo, C. (2011). Accountability online: Understanding the web-based accountability practices of nonprofit organizations. Nonprofit and Voluntary Sector Quarterly, 40(2), 270-295.

Schepers, D. H. (2006). The impact of NGO network conflict on the corporate social responsibility strategies of multinational corporations. Business and Society, 45(3), 282-299.

Shea, C., & Sitar, S. (2004). NGO Accreditation and Certification: The Way Forward? An Evaluation of the Development Community's Experience. Institutional Center for Not for profit Law. Washington. Retrieved on January 2012 from: http://www.usaid.gov/our_work/crosscutting_programs/private_voluntary_coopera-tion/conf_icnl.pdf.

Simar, L., & Wilson, P. (1998). Sensitivity analysis of efficiency scores: how to bootstrap in non-parametric frontier models. Management Science, 44, 49-61.

Simar, L., & Wilson P. (2000a). Statistical inference in nonparame-tric frontier models: the state of the art. Journal of Productivity Analysis, 73(1), 49-78.

Simar, L., & Wilson, P. (2000b). A general methodology for bootstrapping in nonparametric frontier models. Journal of applied statistics, 27(6), 779-802.

Simar, L., & Wilson, P. (2007). Estimation and inference in two-stage, semi-parametric models of production processes. Journal of Econometrics, 736(1), 31-64.

Taylor M., Kent, M. L., & White, W. J. (2001). How activist organizations are using the Internet to build relationships. Public Relations Review, 27(3), 263-284.

Treviño, J. (2004). Las ONG de derechos humanos y la redención de la soberanía del estado mexicano. Foro Internacional, 777(3), 509-539.

Turilli, M., & Floridi, L. (2009). The ethics of information transparency. Ethics and Information Technology, 77(2), 105-112.

Vaccaro, A., & Madsen, P. (2009a). Corporate dynamic transparency: The new ICT-driven ethics? Ethics and Information Technology, 77 (2), 113-122.

Vaccaro, A., & Madsen, P. (2009b). ICT and an NGO: Difficulties in attempting to be extremely transparent. Ethics and Information Technology 77 (3), 221-23.

Valladares, A. M., & Neira, I. (2003). Impacto de la ayuda oficial al desarrollo en Centroamérica. Estudios Económicos de Desarrollo Internacional, 3(1), 1-19.

Vázquez, J. J. (2011). Attitudes toward nongovernmental organizations in Central America. Nonprofit and Voluntary Sector Quarterly, 40(1), 166-184.

Verbruggen, S., Christiaens, J., & Milis, K. (2011). Can resource dependence and coercive isomorphism explain nonprofit organizations' compliance with reporting standards? Nonprofit and Voluntary Sector Quarterly, 40(1), 5-32.

Warren, S., & Lloyd, R. (2009). Civil Society Self-Regulation: The Global Picture. (Briefing Paper No. 119). One World Trust, London. Retrieved on January 2012 from: http://www.oneworldtrust.org/index.php?option=com_docman&task=doc_view&gid=377&tmpl=component&format=raw&Itemid=55.

Waters, R. D. (2007). Nonprofit organizations' use of the Internet: A content analysis of communication trends on the Internet sites of the philanthropy 400. Nonprofit Management and Leadership, 78(1), 59-76.

Wu, I. X., & Zang, J. S. (2009). The Voluntary Adoption of Internationally Recognized Accounting Standards and Firm Internal Performance Evaluation. The Accounting Review, 84(4), 1281-1310.

Xuegang, C. (2004). The Effects of Corporate Governance on Corporate Transparency Experience from China Listed Companies. Accounting Research, 8, 72-80.

Zhongsheng, Z., & Hanwen, C. (2008). Accounting Information Transparency and Resources Allocation Efficiency: Theory and Empirical Evidence. Accounting Research, 12, 56-62.

Cómo citar

APA

ACM

ACS

ABNT

Chicago

Harvard

IEEE

MLA

Turabian

Vancouver

Descargar cita

CrossRef Cited-by

1. Francisco José López-Arceiz, Ana José Bellostas Pérezgrueso, María Pilar Rivera Torres. (2017). Accessibility and transparency: impact on social economy. Online Information Review, 41(1), p.35. https://doi.org/10.1108/OIR-09-2015-0296.

2. Faris Odeh Al Majali. (2023). A conceptual framework for operational performance measurement in wholesale organisations. International Journal of Productivity and Performance Management, 72(6), p.1627. https://doi.org/10.1108/IJPPM-03-2021-0174.

3. Susana Álvarez-Otero, Emma Álvarez-Valle, Mar Arenas-Parra, Raquel Quiroga-García. (2024). Analysis of the ‘Good’ performance indicators of Non-Governmental Development Organizations. World Development Perspectives, 36, p.100639. https://doi.org/10.1016/j.wdp.2024.100639.

4. N. Fadzlyn, Filzah Md. Isa, Shafi Mohamad. (2023). Finance, Accounting and Law in the Digital Age. Contributions to Management Science. , p.55. https://doi.org/10.1007/978-3-031-27296-7_6.

5. Susana Álvarez-Otero, Emma Álvarez-Valle. (2024). The NGDOs Efficiency: A PROMETHEE Approach. Journal of Risk and Financial Management, 17(9), p.382. https://doi.org/10.3390/jrfm17090382.

6. Fanny Dethier, Cécile Delcourt, Jurgen Willems. (2023). Transparency of nonprofit organizations: An integrative framework and research agenda. Journal of Philanthropy and Marketing, 28(4) https://doi.org/10.1002/nvsm.1725.

Dimensions

PlumX

Visitas a la página del resumen del artículo

Descargas

Licencia

Derechos de autor 2016 Innovar

Esta obra está bajo una licencia internacional Creative Commons Reconocimiento-NoComercial-CompartirIgual 3.0.

Todos los artículos publicados por Innovar se encuentran disponibles globalmente con acceso abierto y licenciados bajo los términos de Creative Commons Atribución-No_Comercial-Sin_Derivadas 4.0 Internacional (CC BY-NC-ND 4.0).

Una vez seleccionados los artículos para un número, y antes de iniciar la etapa de cuidado y producción editorial, los autores deben firmar una cesión de derechos patrimoniales de su obra. Innovar se ciñe a las normas colombianas en materia de derechos de autor.

El material de esta revista puede ser reproducido o citado con carácter académico, citando la fuente.

Esta obra está bajo una Licencia Creative Commons: